Welcome to this week’s edition of Cape May Wealth Weekly. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive!

The first version of this article was published on Closing The Gap in March 2024.

Few asset classes have seen as much turbulence in recent years as venture capital. Prior to 2021, we saw “peak optimism”: Soaring valuations, with seemingly limitless funds for fast-growing companies. Today, the world looks very different, both for the start-ups, and for the venture capital funds themselves. But especially when an asset class falls out of favor, it might be the best time to take a close look again.

Together with Johannis and Hendryk of jvh-ventures (and publishers of the fantastic venture capital investing blog Closing the Gap), I want to give you an in-depth view into venture capital as an asset class. Last week in Part 1, we covered the fundamental basics of VC, as well as one of venture’s biggest driver of returns, the so-called Power Law.

Today, we will cover the key concept of return dispersion in venture capital, as well as the resulting importance of manager selection - and finally, we will take a look at how venture capital might play a role in a diversified portfolio.

Manager Selection: Or, how to capitalize on return dispersion

Source: CAIS (November 2022).

Even if this is your first foray into VC investing, you might have some experience investing in public markets. And there, you might’ve encountered the concept of so-called return dispersion: It is the distribution of returns of a given asset class (say, US Equities) relative to its average. Some active fund managers might outperform (i.e. they achieve performance in excess of the S&P 500 (or another US Equity benchmark), while others might underperform. The larger the difference between the outperforming funds and the underperforming funds, the larger the so-called return dispersion.

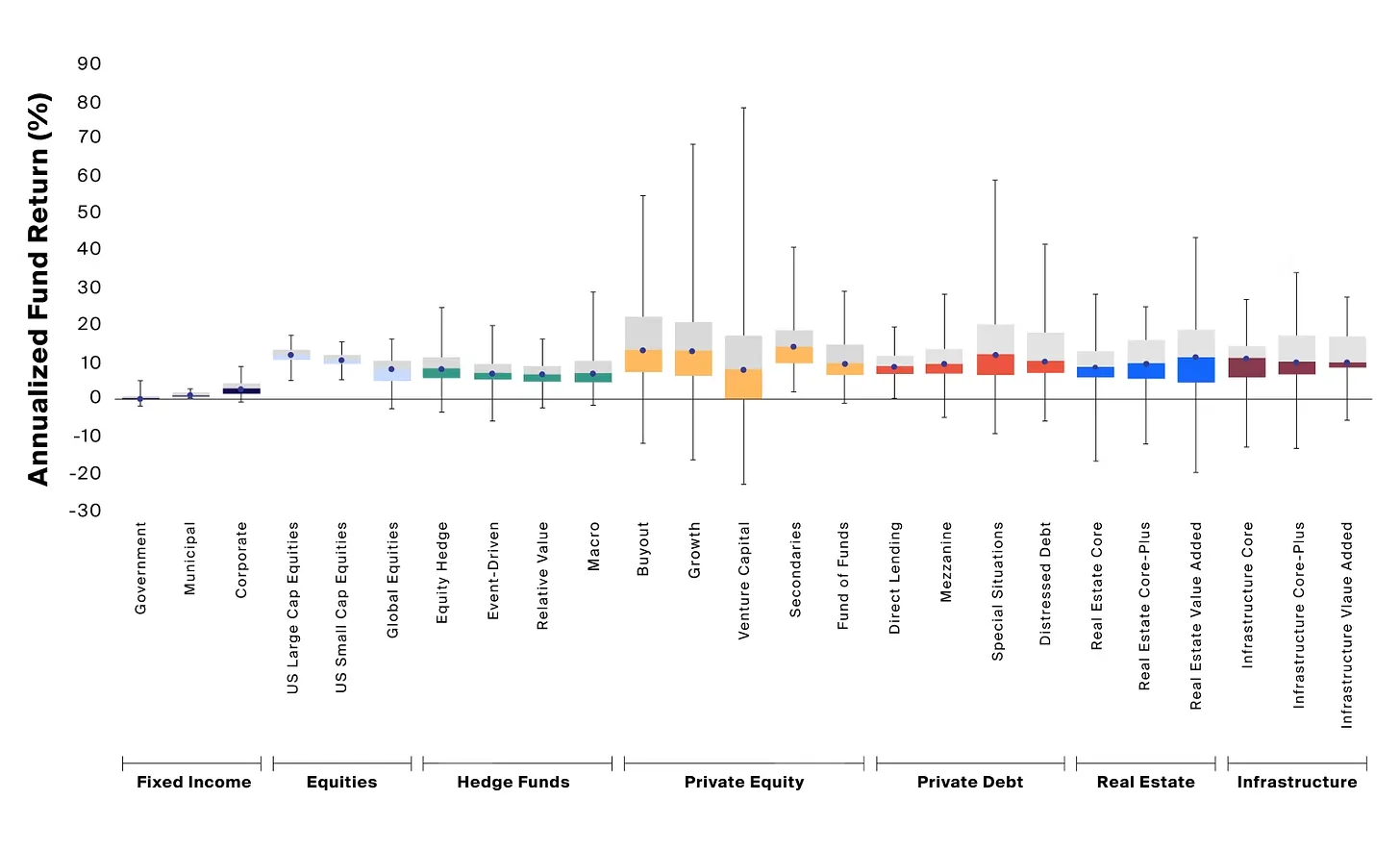

So why should you care about return dispersion in venture? Because the asset class has, by far, the largest return dispersion:

While the average VC fund achieved decent returns relative to the NASDAQ (according to Cambridge Associates, a 16.9% return over the last 10 years ending in September 2023, relative to 14.9% for the NASDAQ), there is a good chance your return was far away from that average. According to an analysis by CAIS from November 2022, using IRRs rather than annualized returns, the median VC fund generated a return of 8.2%. In my experience, IRR for a singular fund tends to be ½ to ⅔ of the annual return, meaning that the median VC fund would’ve only generated 4-6% annualized return.

So why is the gap between the average and the median return so big? Because as we said, VC return dispersion is massive: top-quartile funds generated returns between 17% p.a. (decent!) to 79% p.a. (mind blowing), while bottom-quartile funds saw returns between 0.3% (at least it’s positive) to -22.4% p.a. (terrible). In other words, unlike other asset classes where median and average return tend to be somewhat close to each other, the average return of venture capital is affected significantly by its outliers - showing that the Power Law doesn’t just apply to individual start-ups, but also to venture funds.

And it is exactly this dispersion where so-called Manager Selection skill comes into play. Manager Selection, as the name says, is the skill (and art) of finding managers of which you would hope that they find themselves in the top quartile of managers - or at least, above average. Without trying to calculate any definite examples, it should be clear to most readers how significant the return of constructing a Tier 1 venture portfolio can be. Even at the lower end of the top-quartile fund return, an investor would compound returns at 17% per year after costs, almost twice the long-term average return of most public markets.

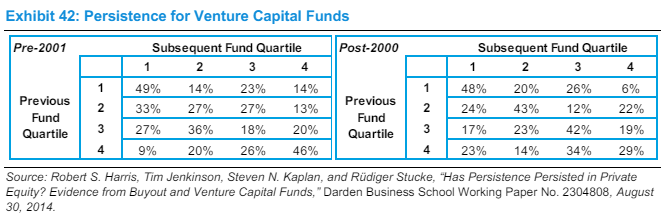

Interestingly, some readers might wonder about hindsight bias here. After all, as I outlined in The Quantitative Approach to Private Equity, there is little so-called persistence in returns between funds. In other words, in the case of private equity, there is no proof that picking managers with a recent first-quartile fund will achieve first-quartile returns for their subsequent funds. Interestingly, in venture capital, the data shows a very different picture (taken from Morgan Stanley’s fantastic paper Public to Private Equity in the USA):

Source: Morgan Stanley.

In other words: A top-quartile venture fund has a nearly fifty percent likelihood of being followed by another top quartile fund. So if you pick a fund manager whose prior fund had such top-quartile returns, you have a very high chance to see similar returns in their subsequent funds.

However, it’s worth noting that accessing top-quartile venture funds is easier said than done. Unlike private equity, where top-performing GPs have aggressively increased their fund sizes to single- and double-digit billion dollar funds, venture capital tends to be more size-constrained. Hence, funds are smaller - but given the aforementioned return persistence, many LPs try to access the same GPs, who end up being able to select LPs to their liking, and often also ask for more aggressive fees and structures.

Investors might still be able to generate good returns from accessing smaller, local managers (who might also have a size advantage on the lower end), but should be mindful of how top-tier GPs dominate overall VC returns. If they can’t access high-quality funds, LPs might actually be better off not investing in VC, instead achieving their tech exposure i.e. through a broadly diversified, tech-focused index fund. Or they could capitalize on someone else’s manager selection skill: In other words, invest in a fund of funds that might have access to said top-tier funds. Given the return dispersion, which disproportionately favors the outlier GPs, it is one of the few areas where the additional layer of fees, in my view, might be worth it. (But the topic of fund of funds is definitely one worth a stand-alone article in the future.)

But no matter if you access funds directly or through a fund of funds, don’t forget the blessing and curse of performance dispersion: In some cases, you might be on the right side of the distribution, resulting in phenomenal outperformance. But equally, you might also see underperformance - and in the case of venture, it might not just be a few basis points, but even a double-digit underperformance, or even worse, a total loss of capital. While first-quartile managers might have a higher chance of being first quartile again, there’s still a significant probability of ending up in the fourth quartile.

The role of Venture Capital in a Diversified Portfolio

So let’s tackle the final question: How should you think about venture capital within your overall asset allocation? Let’s first revisit what we deem to be the key benefits of VC as an asset class:

First, VC allows an investor to invest in disruptive business models and technologies before they move into the mainstream. If we look back at some of the big venture-backed companies of the last 10–15 years, we can see how the mainstream initially didn’t think their business model could succeed given that it was so novel - think companies like Uber, Airbnb or Coinbase. Ideally, this focus on cutting-edge technology also translates into superior returns. However, for many investors, investing into VC and thus innovative business models can be a reward in itself: They don’t just want to see their capital invested into a diversified, impersonal equity ETF, but want to see directly how their capital can generate a positive impact in the world.

Second, VC is a very long-term oriented asset class. As we mentioned above, the long holding period is a result of a fund’s winners remaining in the portfolio to compound value until an eventual exit late in their fund lifetime. The magic word here is compounding: While average IRRs (leaving aside dispersion for now) are actually not that different between VC and private equity, VC ends up having higher fund-level multiples given the longer average holding period. If you are an investor that isn’t dependent on distributions and/or can invest in this part of your portfolio for a long time, there are few other asset classes allowing such long-term compounding without reinvestment (including the associated tax benefits).

Third and last, VC, both at portfolio and fund level, has significant performance dispersion, which rewards investors skilled at manager selection. As we outlined, the gap between top- and bottom-quartile funds is massive. But if an investor can consistently manage to access above-average funds, few asset classes offer such substantial returns as venture. As we mentioned, the Power Law at portfolio level also applies to the fund level, with select funds offering significant outlier returns themselves (think double-digit fund multiples). But of course, as we outlined, that’s easier said than done: Accessing top-quartile managers can be difficult, especially for smaller investors.

Together, those benefits, in our view, point a good picture of when venture capital can be a good addition to a portfolio: In terms of Quantitative Investment Goals, VC makes sense if you are looking to capitalize on (or are dependent on) the significant long-term performance of well-performing venture capital funds (or direct investments). In terms of Qualitative Investment Goals, venture capital can be a good fit if you have a ‘philosophical’ bias towards VC’s tendency to support innovative businesses, and if you are willing and able to develop the manager selection skills required to access top-performing funds.

So those are the benefits of venture capital. But that shouldn’t be your only consideration - you should also consider the risks associated with the asset class. And in the case of VC, those risks are illiquidity and performance dispersion.

Illiquidity tends to be the key consideration, even for those that might have manager selection skills. One VC fund by itself might take ten years to return just its invested capital. If you build a portfolio of funds, where early distributions are used to fund capital calls of other funds, this break-even point moves even further into the future. While selling stakes in a VC fund isn’t impossible, it can be time-consuming and usually comes with substantial discounts to the fund’s underlying value.

Said differently: If the liquidity profile (or said differently, its significant illiquidity) doesn’t match your required liquidity profile set within your Quantitative Investment Goals, VC is likely not the right investment for you.

But even if you are willing to hold onto your investments for that long, VC might still not be the best choice, given the aforementioned performance dispersion. I personally like to highlight the aforementioned figures by Cambridge Associates: As we pointed out, Cambridge’s US VC Index returned 16.89% p.a. over the last 10 years, roughly 2% higher than the NASDAQ. But it wasn’t always this way: If we look at a 15-year period, VC actually underperformed NASDAQ by 1.6% p.a., and was just 0.5% ahead of the index over a 20-year period. And let’s not forget that your NASDAQ ETF can be sold daily, whereas your VC fund is extremely illiquid.

Using the Investment Objective Framework for one final time, those are risks that fall both into the Quantitative Investment Goals (required performance relative to your risk objectives) and your Qualitative Investment Goals (operational preferences and complexity). Anyone looking to invest in venture shouldn’t expect the outlier returns, but the (somewhat disappointing) average or median return. And using those figures, you need to ask yourself whether this level of outperformance (or lack thereof) is worth the effort, complexity and liquidity. Once again, if the question to this answer is no, we advise to stay away.

But if you are able to stomach the illiquidity, and think you can build access to top-tier funds (or at least a good fund of funds), venture capital can definitely be a great addition to your portfolio. The compounding effects are significant, long-term returns can be tremendously attractive - and there is one last benefit, from personal experience: It can be a lot of fun.

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.