Welcome to the very first edition of Cape May Wealth Weekly. If you’re new here, subscribe to ensure that you receive my next piece in your inbox, and of course, tell your friends about this amazing new newsletter launch. 🚀

Most investors start their investing journey backwards - meaning that they make an investment, and later see how it fits into their portfolio. (If they even ask themselves this question). Yet while most investors usually have a rough idea of what they are trying to achieve (and how their portfolio should look like), few have actually spent the time to systematically and holistically think about their investing objectives. I want to help bring clarity into this matter - so in this article, we will explore the questions that investors should ask themselves before they get started in order to better understand what they want to achieve, and how they can achieve it.

There are four areas that we will focus on: Investment objective, return goals, risk goals, and finally, personal preferences. Let’s begin - I hope you find it helpful.

Investment Objective

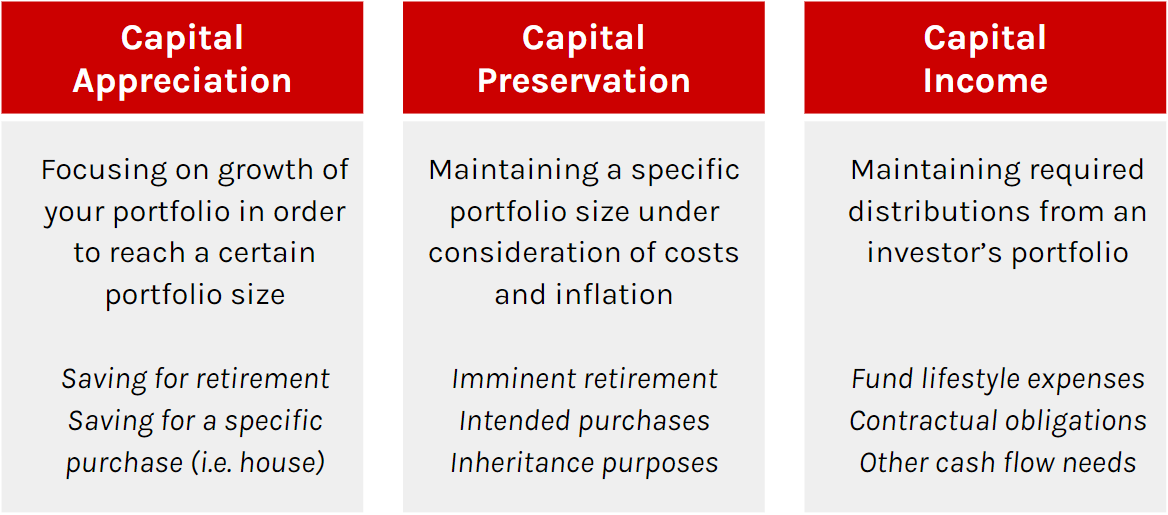

To me, the Investment Objective is the overall goal that a client is looking to achieve through their investing activities. There are three options that I present to my clients: Capital Appreciation, Capital Preservation, and Capital Income. What do they entail?

Conveniently, the three objectives also roughly describe how individuals invest over their lifetime - starting by growing their assets through savings and returns, maintaining that portfolio once they reach their target portfolio size, before then drawing income from the portfolio once they decide to retire.

It is important to note that the objectives are not mutually exclusive. An investor focused on growing their portfolio might also want to ensure that the portfolio’s potential loss in a drawdown is limited (i.e. capital preservation), or an investor looking to draw income might still be return-oriented in some parts of their portfolio. Accordingly, only few clients make the clear decision to focus on just one of the three, but rather try to find the trade-off between the three that best fit their individual needs. One should however be mindful of this trade-off: For example, focusing on income too early might reduce the “capital stock” of your retirement portfolio, which can bear risks in regards to sufficient funds for later in your life, or focusing on capital appreciation late in your life might result in drawdowns that can endanger the capital stock that you are drawing from to fund your lifestyle expenses.

Admittedly, asking this question is very simple - so why do I still ask it? Not just for the answer, but to hear why a client chooses an objective. In answering the questions, clients provide me with the background, experiences and “story” of why they have decided that way - and in doing so share information to help me shape the process, but also highlight potential conflicts between their choice and the realities of investing.

What conflicts do I mean? More on that in the next section.

Return Goals

Most people invest to make money. Accordingly, asking someone for their return target usually gets the same answer: As high as possible, of course. But while most people are aware that higher returns bring higher risk, few stop and ask themselves two questions I like to raise: What type of return they are looking for, and why they want to maximize returns (as opposed to other factors) in the first place.

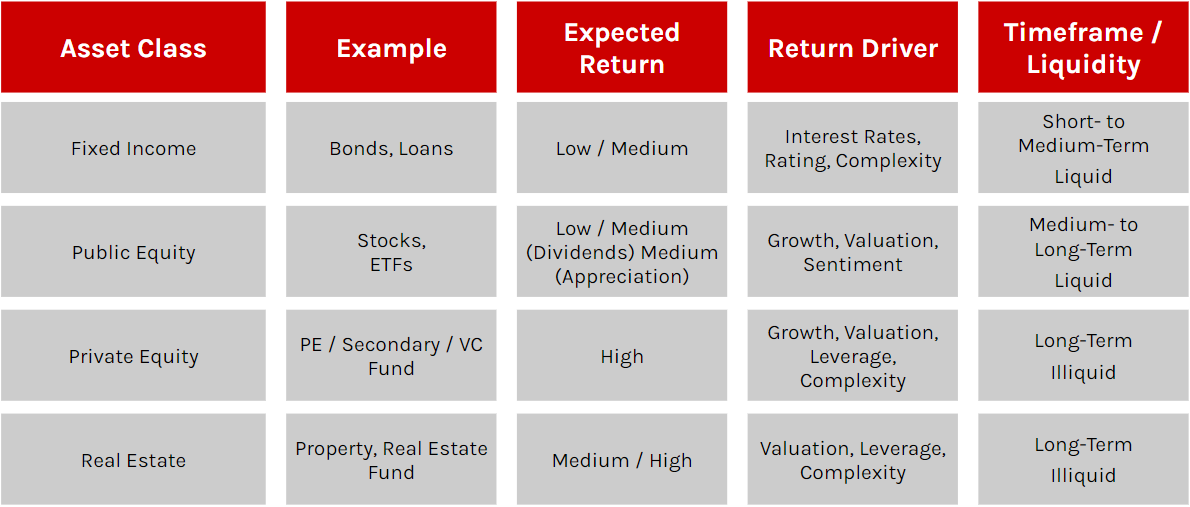

Let’s begin with the type of return. While all returns grow your portfolio, their “origin” is fundamentally different by asset class, as you can see below:

One thing is clear: High returns don’t come quickly, but are the result of long-term orientation, complexity,and/or illiquidity - and even the most return-driven investors might not be willing to accept 100% high-risk, illiquid investments. Also, as portfolio theory teaches us, combining assets with a lower expected return might result in a higher long-term return than an individual asset with higher expected returns, which might feel counterintuitive.

More importantly, however, is the question of WHY an individual might want to maximize their returns. For some clients, non-financial aspects to investing such as ESG or personal preferences might have importance over maximizing performance. However, that is not necessarily even what I want to address here. Rather, let’s focus on the “cost” of trying to achieve excess returns.

Let’s say you aren’t satisfied with the ~7% p.a. equity return even though it’s sufficient to achieve your retirement goals. What assets have historically offered excess returns? Illiquid ones, such as private equity or real estate, where there are no index funds, and where accordingly you are required to pick individual managers - which is far more complex than buying an ETF: Before you invest, you need to source and screen managers, and need to evaluate and execute their contracts and solve structural questions such as taxes. Once you invest, you need to manage cash flows, track fund performance, and deal with ongoing complexities, such as reporting. Depending on how you invest, a later divestment might also consume additional time and money.

However, there is no guarantee that all this work actually pays off: Alternative investments have significant “return dispersion”, meaning the difference of returns between funds that perform well and those that do not perform well. And while everyone thinks that they can pick the top 50% of funds, the laws of statistics tell us that someone will end up with the bottom 50%. Lastly, even if you pick a well-performing fund, you also have to look at the (relative) effort again: Is the outperformance sufficient to justify the additional work required to source and manage your investment? Especially if an investor can achieve their target returns through more simple products, they should seriously ask themselves the question whether the potential excess returns are worth the effort. In more than one case, I’ve seen investors end up “dabbling” in alternative investments before returning to less complex, liquid investments that are also sufficient to generate their target returns.

So if you don’t want to spend the time to optimize your returns beyond what is necessary, how should you spend your time? On the other side of the equation: Risk.

Risk Goals

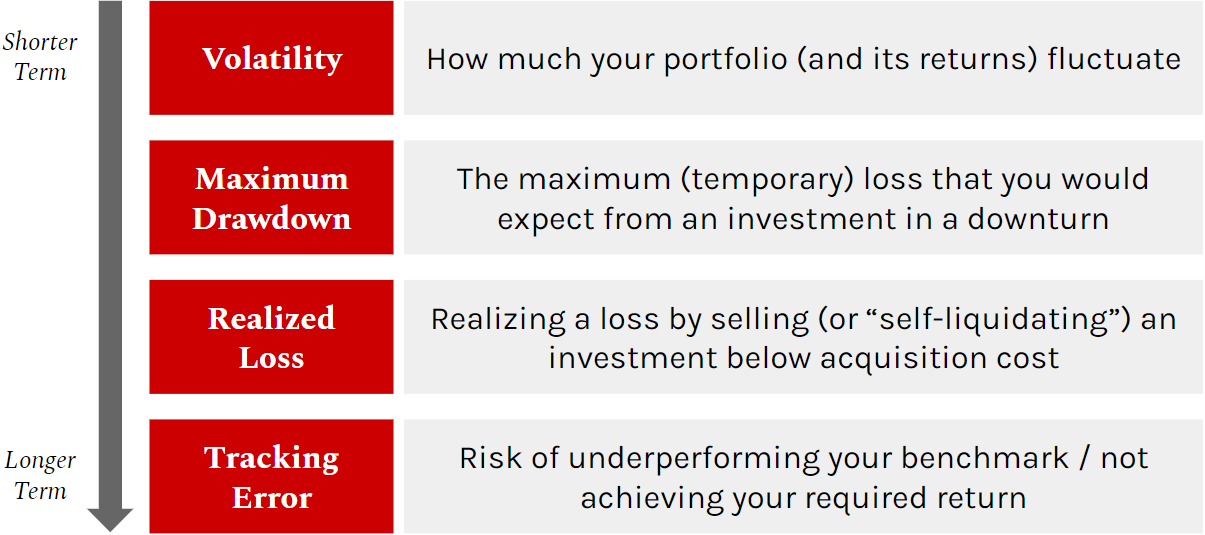

There are four ways of how I look at risk:

To make those examples a bit more practical:

Volatility: Public market investment usually doesn't just go up in a linear fashion, but fluctuate driven by market events as well as things that happen to the underlying company (or companies). If you’re a long-term investor, such fluctuations don’t matter as long as the long-term trajectory is positive. However, if you are dependent on selling your investment at a certain point in time for a certain minimum price, volatility is a real risk for you, as these temporary fluctuations might depress the price of your investment.

Maximum Drawdown: Maximum drawdown shows what potential paper loss an investment might incur during times of market volatility. For example, during COVID, public equities saw drawdowns of up to 20% to 30%. Over a given time period, the maximum paper loss from peak to through is called the maximum drawdown. Once again, if you are a long-term investor, this matters less to you. If you are more short-term oriented, things look differently - if you invest 100€ today and want to make sure you always get at least 50€ back, you should pick investments for which you would not expect a maximum drawdown of more than 50%.

Realized Loss: Realized loss is the risk of not being able to sit out a temporary drawdown of an investment, but actually crystallizing this investment into a real loss. This can for example happen if you invest into a singular company (either private or public) that ends up bankrupt. It can also happen in the case of financial derivatives, which might not be “in the money” on their expiration date. Depending on the investment, realized loss might be less of a relevant metric - for example, if you buy an equity index fund, companies might go bankrupt, but are then replaced by other companies. Accordingly, it’s less likely (although not impossible) to face an unintended realized loss unless you sell the instrument yourself. If you are an investor that is sensitive to realized losses (as opposed to just temporary drawdowns), you might be more mindful of which investments are right for you, and which are not.

Tracking Error: Tracking error is the risk of underperforming your set benchmark and/or target return over a designated period. For example, if you are a retail investor who requires a 7% return on your investments per year to reach your retirement goals, but only achieve a 6% return, your goal is in serious danger unless you source additional capital. But even without a return goal, tracking error is relevant - you might face the risk of your non-passive investments, for example private or public equity funds, underperforming the benchmark. Tracking error is less relevant over short time periods, but incredibly important over long periods, as even slight deviations from benchmark or return goals can compound to significant sums.

Which of those risk factors is relevant for you? That depends on your investment objective:

Investors focusing on capital preservation look to minimize their potential maximum drawdown and avoid investments that might force them to realize permanent losses.

Investors focused on capital income might care less about drawdowns, volatility or tracking error, as long as their portfolio provides the required ongoing level of income.

Investors focused on capital appreciation don’t care about volatility, maximum drawdown or even short-term realized losses as long as their portfolio generates the required long-term returns.

Accordingly, individuals looking to think about risk should see how their overall investment objective affects what risks they should avoid, and which ones they are able to stomach.

Personal Preferences

Lastly, let’s review the last, but not least important point: Personal preferences. While there are likely more, I like to divide them into three categories.

First, “Philosophical” Preferences. Here, I include all non-financial factors that affect an investor’s investment decisions.

One frequent point is ESG, where investors exclude or highlight investments that are aligned with their personal preferences around those three factors. However, there are also “non-moral” personal preferences around asset classes or strategies. For example, I know some German clients like real estate as “Betongold” (concrete gold). Other clients dislike hedge funds for their intransparency and complexity. But there are many more factors, such as how involved a client wants to be in their investments.

In my view, there is no right or wrong to either of these answers, and I try not to impose any personal preferences on those views onto my clients. Nevertheless, I find it important that investors are reflective on those matters, especially when it comes to positive preferences. For example, I find that many tech entrepreneurs have a natural inclination for venture capital investments - but in many cases, while they have made money in the asset class and have a lot of experience in it, it might actually not be a good fit relative to their investment objective and risk goals.

Second, Operational Preferences. It takes little time to start investing, but much more time-consuming to manage a portfolio. Accordingly, investors need to make the decision of “in- vs. outsourcing”, i.e. taking care of investment matters themselves, outsourcing them to advisors, and/or even setting up their own family office. There are reasons for and against either choice, but it needs to be prudently made in order to avoid a rude awakening: More than once have I seen investors take care of their investments on their own only to realize they’re spending more time with partnership agreements and tax advisors than the actual task of investing.

Third and last, Complexity. The world of investing offers an almost unlimited level of complexity - but complexity is not necessarily good. That goes back to what we discussed earlier about return targets: Many affluent investors like the idea of illiquid investments for their additional return, but underestimate the complexity and risk that such investments bring - especially when “plain vanilla” products are expected to generate the same return. But even if an investor is aware of the risk-return-ratio of illiquid investments, there are additional variations, for example between investing in funds or investing in such asset classes directly, which might bring even more upside risk but also more work.

What’s the right Investment Objective for me?

The answer is simple: There is no right or wrong approach - it’s the one that best fits your goals, experiences and desires.

We often read in financial media that a certain investment or asset class is the place to be right now. Right now, it’s AI, previously, it was crypto. Sometimes, such “predictions” might be true - and investors, both new and old, try to see how they can implement such trends into their portfolio.

To me, that is the wrong way to go. The much better way is to think about your goals first: Mapping out what you want to achieve, thinking about how much risk you want to take, and considering which asset classes are right for you. The result is a framework that makes it much easier for you to elaborate trends, as any new trend can then be evaluated against your own answers:

AI: Accessible through venture capital investments. Venture capital requires significant manager selection skills, and is very illiquid - does that align with your goals?

Crypto: Accessible through tradeable tokens - which are extremely volatile and face a significant drawdown risk. Are you willing to bear those risks relative to the expected (yet uncertain) return?

Accordingly, my recommendation to you: Take the time, maybe even a weekend, to answer those questions for yourself. Put them aside, and review them critically a week later. I promise that the effort is worth its time.

Liked what you read? If you enjoyed this piece, make sure to subscribe to not miss out on future pieces, and to tell your friends and colleagues about it. I write about topics covering the world of family offices, asset allocation, and alternative investments. More to come next week.