Welcome to this week’s edition of Cape May Wealth Weekly. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive.

The first version of this article was published on Closing The Gap in March 2024.

Few asset classes have dominated the public discourse as much in recent years as Venture Capital (VC). During the days of low interest rates, investors tried hard to get as much capital deployed into the asset class as they could - financing capital-intensive business models ranging from electric cars to quick commerce just before they had the chance to go public via IPO or SPAC.

Three years after “peak optimism” in 2021, things look very different. Many of the praised companies that ended up going public trade at a fraction of their initial valuations, or have even gone out of business. Private start-ups are struggling to maintain their lofty valuations. And even the Venture Capitalists are having a hard time raising capital for their next funds.

Investors that only started investing in VC in 2021 might be unsatisfied with performance so far, with future allocations in significant doubt. But maybe it’s exactly during these gloomy days that we should consider a closer look at VC as an investment opportunity.

Together with Johannis and Hendryk of jvh-ventures (and publishers of the fantastic venture capital investing blog Closing the Gap), I want to give you an in-depth view into what venture capital is: From its fundamental basics, to its role in a portfolio, and lastly, how you can access the asset class (assuming that it is right for you).

Back to the Basics: What is Venture Capital?

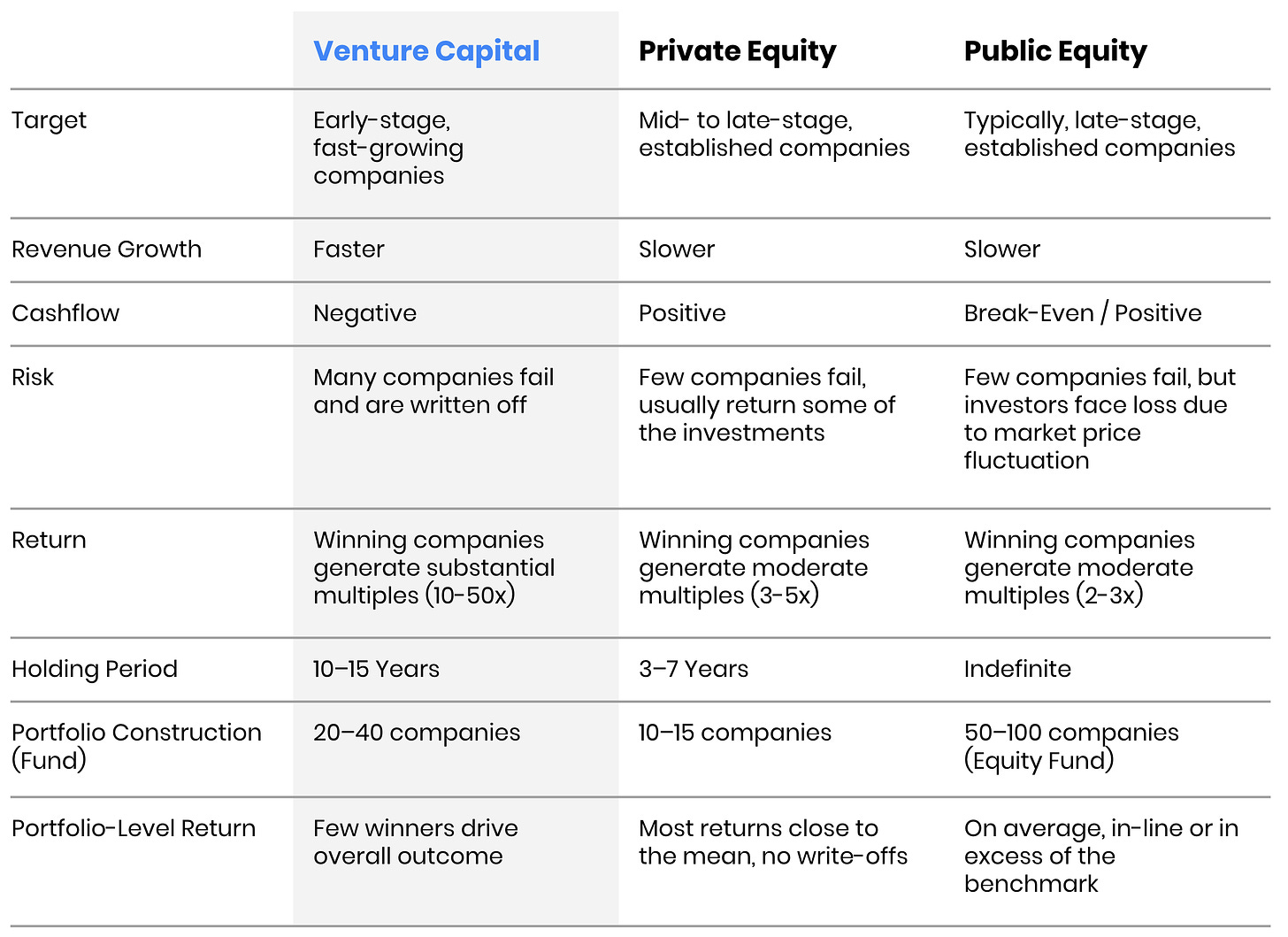

The investible scope of VC is quite large, ranging from idea-stage businesses in a garage to late-stage, giant software companies. However, its key premise is usually the same: Investors in VC aim to make minority investments into young, rapidly-growing companies looking to become the next leader in their respective fields.

The companies that VCs invest in usually have little or even no revenue and high costs for technology, marketing and people, resulting in negative cash flow. VCs solve this issue of negative cash flow by providing growth capital, allowing those companies to reach the next step of their growth journey. This growth capital is typically provided as equity, meaning that with each financing round they provide, VCs acquire a stake in the underlying business. They hope to monetize this stake at a later point in time, either by selling their stake partially (a “secondary transaction”, where just the VC might sell a stake), entirely (for example through a sale of the entire company to a strategic or financial investor), or by taking the company public through an Initial Public Offering (IPO).

While the time to exit might vary depending on the “stage” of the underlying portfolio companies (i.e. how mature the company is, so just founded or close to IPO), VC is for the most part a long-term game. If you are an early stage investor, it might take five, ten or even 15 years until your portfolio companies are sold - in particular, if the company does well, in which case VCs are usually advised to let their winners ride rather than to sell them early. Accordingly, even among other illiquid asset classes such as private equity or hedge funds, VC is extremely illiquid. Any investor in the asset class should expect a single fund to pay back its invested capital 8 to 10 years after you made the investment, with the actual returns more likely to be distributed somewhere between years 10 and 15.

Last, but not least, probably the most important point about investments in early-stage startups: They face a significant risk of total loss of capital. Nascent technologies might not find “product-market-fit”, hard-working teams might fall apart over personal issues, or companies might simply run out of money. Accordingly, most start-ups fail, resulting in partial or full write-off of a VC’s investment. This, however, is offset by the success of the few substantial winners: VCs that invested early into companies such as Uber or Airbnb generated double-, if not triple-digit multiples on their invested capital.

This logic is called the “Power Law”, in which a small percentage of start-ups generate the lion’s share within a VC portfolio. At JVH Ventures, around 8% of the best companies return more than the rest combined. However, this might be a rather large share of winning companies on average, as VCs normally calculate with 1-2% of funds returning outlier startups in their portfolios' construction. JVH Ventures might not be representative here, as they both have lower rate of losses and the portfolio is still rather young.

Accordingly, it is critical to remember that in VC, a substantial portion of direct investments fail or generate just minor returns - making it necessary for investors to construct a sufficiently diversified portfolio. (For a great deep-dive into the mechanics of venture portfolio construction, take a look here.)

For better understanding, let’s put this into comparison:

The Power Law: Understanding Venture Capital’s Key Return Driver

Investors should be particularly mindful of how the potential return outcomes affect a VC or PE fund’s portfolio construction. Let’s first look at Private Equity: For worse-performing deals, a PE fund would always try to ensure that this deal returns its invested capital, i.e. a 1x multiple. For well-performing deals, the target multiple is lower than in VC, usually ranging around 3-5x. However, most deals are expected to come in somewhere between those two figures, typically between 1,5x and 3x. Given this tighter return distribution, PE funds can build concentrated portfolios of 10–15 companies without running the risk of building a loss-making portfolio at fund level.

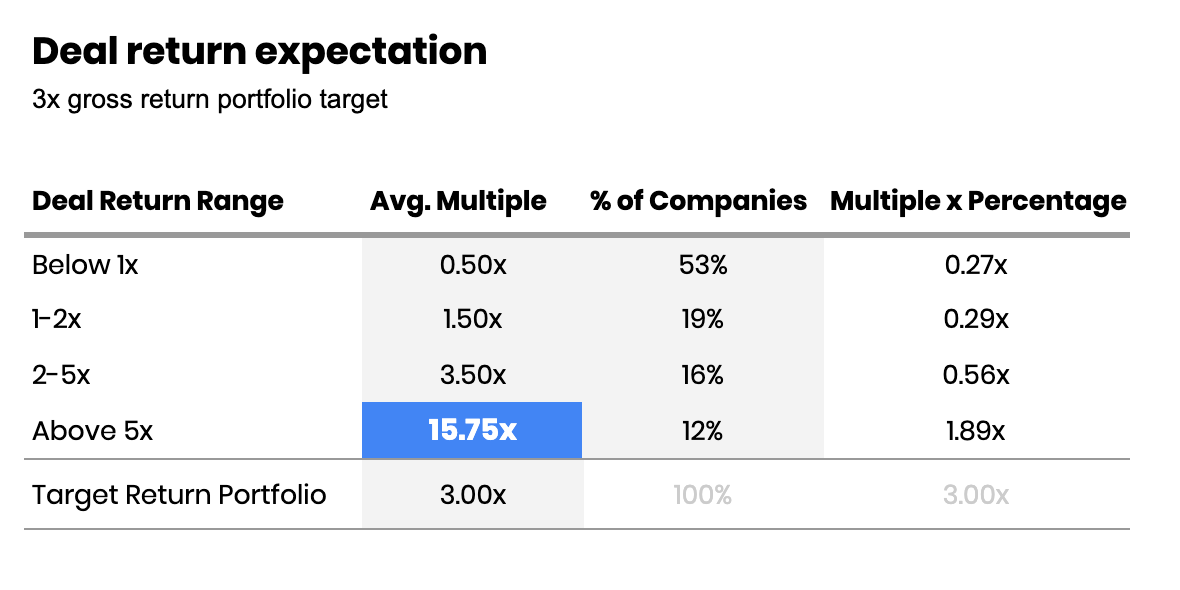

In VC, things are very different. As we explained, a significant number of start-ups fail to produce relevant returns. But how do these company-level figures translate to the portfolio level? To do so, we can look at the data shared by David Clark of the Venture Fund of Fund VenCap. Let’s first again look at the worse-performing deals. In the case of VenCap, 53% of their 11,350 (indirect) portfolio companies failed to generate returns sufficient to return invested capital (and VenCap, which has been around since 1986, is likely picking above-average fund managers, which might have a positive effect on their loss rate.) Before even diving into the return expectations for well-performing deals, we can already see the Power Law in action: To generate a fund-level multiple of 3x or better before fees, the remaining 49% of deals need to generate significant returns to offset deals on which VCs lose money.

What does significant mean? We can again see this in VenCap’s data. In their funds, 19% returned between 1 and 2x, 16% returned between 2x and 5x, and 12% of deals returned more than 5x of invested capital. If we want to achieve a 3x multiple before fees, we can use simple math to calculate what average returns the “Above 5x” deals need to generate:

Return Range and % of Companies based on VenCap Data as outlined above. Avg. Multiple estimated as average multiple within the mentioned range. Target Return of 3.00x based on typical Target Multiple of a VC Portfolio (before portfolio-level fees), i.e. a 3.00x “gross return”

Hence, using Vencap’s figures and our target return of 3x (before fees), the remaining 12% of the fund would need to generate an average return of ~15,75x to reach its 3x target return.

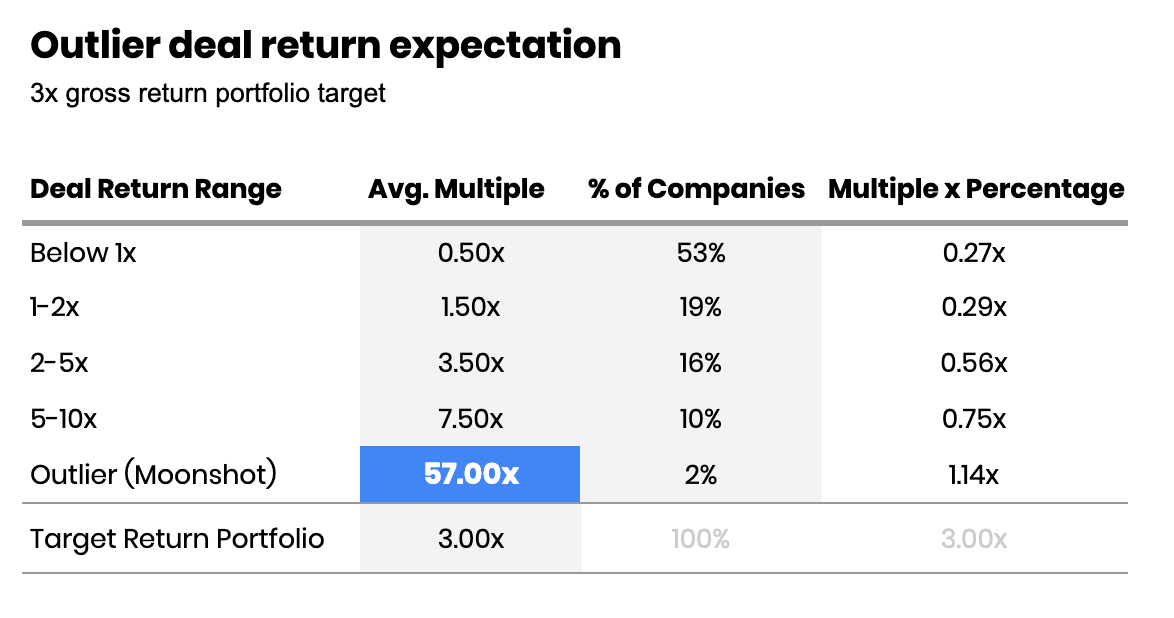

With a typical VC fund consisting of 30-40 portfolio companies, that would mean that we have ~3-4 portfolio companies with this double-digit multiple. Realistically, however, the distribution is even more extreme, where just one portfolio company (~2% to 2.5% of the fund) drives a substantial part of the fund’s performance. This is also consistent with the return expectations of a VC fund, which tries to size (and value) its investments in a way so that a single deal, if it’s a home run success, can return the entire fund.

We can extend our prior table, and once again use simple math to complete the calculation:

Return Range and % of Companies based on VenCap Data as outlined above. Avg. Multiple estimated as average multiple within the mentioned range. Target Return of 3.00x based on typical Target Multiple of a VC Portfolio (before portfolio-level fees), i.e. a 3.00x “gross return”. Breakdown of prior “Above 5x” bucket (12%) into 10% of 5-10x returns and 2% “Moonshots”.

In other words, if we assume that 10% out of the 12% in VenCap’s “above 5x” multiple achieved an average return of 7,5x, that would mean that our remaining single deal (i.e. 2% of the fund) would need to achieve a staggering 57x (!) return for us to achieve our performance goal of 3x.

This outlier-driven nature of VC has a profound impact on the distribution of VC fund outcomes, and accordingly, the performance of VC in investor portfolios. Some outliers can drive significant returns, even in excess of this hypothetical 57x multiple. But likewise, the absence of an outlier return means that the fund will struggle to achieve its desired returns.

To understand how this impacts you as an investor, let’s take a look at two key concepts in venture capital fund investing, return dispersion and manager selection., and finally, the role of venture capital in a diversified portfolio. Next week, in Cape May Wealth Weekly.

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.