Welcome to this week’s edition of Cape May Wealth Weekly.. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive!

How do you track the performance of your portfolio?

If you are lucky, you might ‘just’ have a singular brokerage account, which does the work for you. It automatically adjusts performance based on end-of-day market prices, as well as inflows and outflows in and from the portfolio.

Things are more complicated if you are investing beyond a singular brokerage account. Commonly, I see affluent investors with multiple accounts, cash accounts with multiple banks, and illiquid investments such as real estate or venture capital. Few tools are able to properly account for all of those different categories. In the absence of easy, affordable tools for wealth reporting for affluent individuals, you might decide to track your performance in a spreadsheet. An absolutely fair choice, and one that I’ve made before for clients as well.

But as always, there’s things to watch out for. Today, let’s talk about Wealth Reporting 101: Better ways to get an overview of your total net worth, and ways to calculate the performance of your portfolio.

#1: Wealth Overview

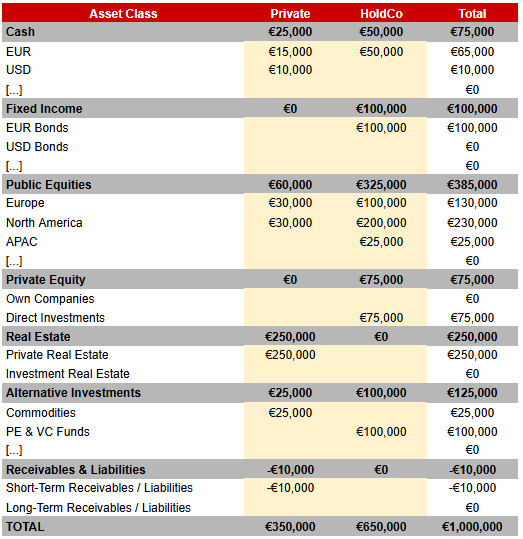

Before we can try to measure the performance of our overall wealth, we first need to know what our overall wealth is. More precisely, we need to have an wealth overview: Typically, some sort of spreadsheet showing us a list of your different assets, divided by bank relationship and entity (i.e. private or company level).

The overview that we use as a starting point to help our clients at Cape May looks something like this - with more detail on the asset class side and the private/HoldCo side as needed:

Source: Cape May Wealth. Figures for illustrative purposes only.

Of course, there’s also more detail behind the sheet, as needed. I personally like to break this overview down by bank/asset management relationship (especially in the case of managed accounts) to more easily see the differences and/or overlaps between the respective strategies. If relevant, we also collect more information about fund investments and their associated cash flows over time (a complex topic, as recently covered in the newsletter). But for the purpose of our analysis, that level of detail isn’t necessarily needed (yet) - an overview like the one above is sufficient.

#2: Multiple on Invested Capital

We have our wealth overview with illustrative figures for further use. With this on hand, let’s start with the most simple method: Multiple on Invested Capital (MOIC).

The formula is as simple as it gets: You divide the current figure of your overall wealth with a historical figure of your overall wealth - historical typically being your initial investment. Take our figures above where the portfolio value currently stands at 1M€. Assuming we began our investing journey with 800k€, our MOIC calculation would simply be:

MOIC = 1.000.000€ (Current Figure) / 800.000€ (Starting Figure) = 1,25x

Simply said, we were able to calculate that our investment currently stands at 1,25x (or a 25% gain) of the initial investment. A positive figure is a great outcome, of course. But there comes the first challenge - assessing whether that 25% gain is meaningful.

How do we do that? Most importantly, we should see that 25% gain in the context of the time period over which it was achieved. For a diversified portfolio as the hypothetical portfolio above, a 25% return over one year would be outstanding, but over ten years, not so much. For any period greater than one year, we can calculate our Compound Annual Growth Rate (CAGR) to see the annual (compounding, not average) return required to achieve our result. For a 10-year investment period, the formula is as follows:

CAGR = [1.000.000€ (Current Figure) / 800.000€ (Starting Figure)]^(1/10 (Investment Period in years)) - 1

CAGR = 125%^(1/10) - 1 = 2,3% p.a.

So if we realized a 25% gain over 10 years, our annualized performance would’ve been 2,3% p.a. - not so great. Hopefully in your case, a 25% gain is over a shorter time period.

#3: Performance over Time

You might think that that concludes the challenges of tracking performance over time - but unfortunately, it’s not so easy.

Let’s go back to our example: Assume that today, our hypothetical portfolio is valued at 1.000.000€. We also know that 10 years ago, we started with 800.000€. Using what we learned about MOIC and CAGR, we would think that our annualized performance should be 2,3% p.a. And that is indeed one of the possible answers. But there is one common complicating factor that people disregard: Inflows and outflows.

Inflows and outflows are especially relevant when assessing parts of your overall portfolio, for example, a singular bank relationship. Take our hypothetical figures again: Things could be as simple as that we wired 800.000€ to that bank, and that 800.000€ has since grown to a million over a 10-year time period. But capital is rarely that static, especially in the world of affluent individuals: Capital is withdrawn to be invested elsewhere or for private lifestyle needs, or (re-)invested with the banks after a direct investment is sold.

Take the following (once again hypothetical) time series:

Source: Cape May Wealth. Figures for illustrative purposes only.

We can see that this time series matches our simple calculation from #2: We start with 800.000€ and we end with 1.000.000€. Over the full 10-year period, our inflows stayed 800.000€ and our performance was 200.000€ - just like in our MOIC calculation. Using those figures, we’d also show a full-period MOIC of 1,25x. But of course, what our MOIC calculation does not show is the substantial swings in the portfolio balance in each period, which is driven by performance as well as our capital flows.

To get an accurate picture, we first need to calculate the performance at the level of each year. To get the performance figure for a given calendar year, we have to divide our Ending Amount by the Starting Amount, the latter adjusted for Inflows / Outflows. If we take our first year from the table above, it goes as follows:

Year 1 Performance = 820.000€ (Ending Amount) / [0€ (Start Amount) + 800.000€ (Inflow)] -1 = 2,50%

We can then repeat the same calculation for each individual period, as visible here:

Source: Cape May Wealth. Figures for illustrative purposes only.

On first glance, it becomes clear that our performance isn’t necessarily as linear as we had initially assumed. Swings range from -10,53% to +13,64%. And secondly, we also see that there’s a difference in our compounded performance: To calculate it, we multiply each of our annual performance figures +1, i.e. (1+2,5%) (1+2,78%) etc. As a result, we get to a slightly different figure of 21,71%, more than 3% lower than our simple MOIC/ROI figure. You might think that that’s a minor difference for a 10-year period, and I wouldn’t disagree - but you get the gist: The numbers are different if we move to a more granular level, and I could adjust the figures above to still show a 25% ROI but a more dramatic difference in compounded performance.

Wealth Reporting 201

If you were able to follow my explanations and calculations until now, and have set up your wealth reporting according to that logic, congratulations: Your performance tracking sheet is more detailed than that of most investors, and even more detailed than that of some family offices.

But of course (and unsurprisingly for a newsletter that I try to keep shorter rather than longer every week), there’s always more to be done.

First, the Asset-Class View.

The two-step process as outlined above - from portfolio snapshot to performance over time - is easy to be done at the level of your overall portfolio. Conduct a regular snapshot, i.e. monthly or annually, check if there were any notable inflows and outflows, and use that to calculate your overall portfolio-level performance.

But take our overview from section #1: We have assets at the private level, and at the company level. We have liquid assets such as bonds and public equity, as well as illiquid assets such as a stake in our own business or an investment in a PE fund. We also have privately used real estate, which factors into the total wealth, but might technically not be a performance-relevant asset.

From experience, I can tell you that this level of granularity where spreadsheet-based tracking tools get to their limit. To get an accurate result, you have to start tracking the movement between different asset classes according to your chosen frequency (monthly, annually, etc.), which includes not only investments (i.e. capital calls and distributions, a new direct investment), but also the associated expenses (which impact performance). That, in return, means you should ideally assess every single transaction on your bank accounts - which might be quite complex depending on your setup and asset allocation (entities, asset classes, etc.). As an entrepreneur (or entrepreneurial family officer), you might think that an 80/20 approach is the right way to go here, but from my personal experience, I can tell you that that makes it even more complicated. It is unfortunately easier to track and validate all transactions rather than just a subset.

Second, Actionable Conclusions.

Imagine you set up a perfect asset class-level view for your various entities (perhaps using a software tool or a service provider). You’re now blessed with perfect, regular insights into the performance of each asset class. But how do we then use that data - what analysis should we conduct?

If your overarching goal, for example, is to achieve a certain target return, even a basic wealth reporting tool should be able to show if you are hitting that goal. But more importantly is the ability to look ‘under the hood’ to see what actually caused you to (not) hit that goal. That, in return, might include analytical processes such as performance attribution (which asset classes contributed what absolute / percentual return to my portfolio-level return) or benchmarking (how did an asset class perform relative to a comparable index or investment). In the end, what analysis to conduct or what KPI to look out for depends heavily on your Investment Objectives - and that is typically an entirely unrelated workstream to your Wealth Reporting setup, although it might give you an overview of what to work with.

And of course, the analysis is only one piece of the puzzle: Tracking your performance, and relevant KPIs, is of no use if you don’t also have processes to then act on (not) achieving certain goals. If we are able to track the performance of our public equity portfolio, and our tool shows us that we are underperforming due to a choice that the portfolio manager made, we should also have a process in mind on how to deal with that ‘breach’. Practically, such decisions of course are not purely binary, and often include quantitative and qualitative factors. But regardless of that ‘human component’, we need to have a process, as otherwise, our level of granularity might not be worth the effort and time.

And that is admittedly a valid question. If you don’t need that level of detail, or simply have a portfolio that is not at that level of complexity - there is no need for a software tool, let alone a massive spreadsheet. If anything, especially in regards to being able to draw actionable conclusions, less is definitely more.

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.