Welcome to this week’s edition of Cape May Wealth Weekly.. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive!

If you’re reading this newsletter, there’s a good chance that you are actively investing in private equity, venture capital, and other closed-end funds (or at least find them interesting).

There are many reasons that might’ve brought you to fund investing, but more often than not, the primary driver is the expectation of long-term outperformance over public equities, provided to you as a trade-off for taking on multi-year illiquidity.

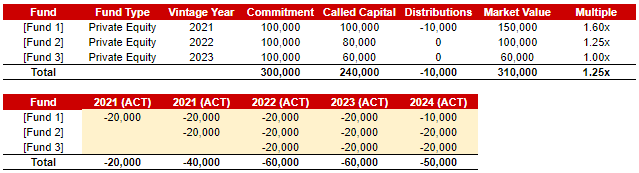

What does the overview over your fund investments look like? Based on the experience working with investors ranging from affluent individual to family office, the answer is often something like this:

Source: Cape May Wealth.

And for the purpose of performance tracking, that overview is, in my view, perfectly fine. Sure, you can do a more nuanced tracking, like quarterly fund- and portfolio-level IRRs or a “public-market equivalent” benchmarking to your equity portfolio, but an overview like above (and its simplicity) is enough if you feel like it's enough.

But an overview like the above is definitely not sufficient when it comes to the biggest risk I see for fund investors - liquidity planning. The typical entrepreneur that I work with has a very high risk tolerance and hence, often a strongly return-oriented portfolio with a significant allocation to illiquid assets. That in itself isn’t an issue, but if you pair it with a) an equally return-oriented (and thus risky) liquid asset portfolio and b) an insufficient overview over your liabilities (both from funds and other assets), things can get problematic very quickly.

When you find yourself with outstanding capital calls but no liquidity, there’s little solace in the value or the exit prospects of your other illiquid assets. So let me help you mitigate that risk: Let’s talk about the best practices of capital call management.

Gathering Our (Historical) Data

Any analysis is only as good as the underlying data. Hence, before we can model our fund portfolio cash flows, we first need to make sure we have all of the required data.

My overview above already shows a few data points - let’s explain why we care about them:

Commitment: The most important figure, showing the maximum dollar / euro amount you have pledged to invest in the given fund. If you committed 100.000€, as in the example above, that is the maximum amount you might have to pay to the fund. Practically, many funds don’t call this amount entirely, and/or are able to offset some of the actual drawn cash with early distributions.

Called Capital: The part of your commitment that the fund has already drawn, i.e. how much money you have wired to the fund. As our liquidity analysis is forward-looking, knowing the current amount of called capital helps us as we can calculate how we need to think about uncalled capital.

Distributions: For the sake of our model, historical distributions aren’t so helpful, as our model is (as I had mentioned) forward-looking. Nevertheless, distributions early in a fund lifetime can be indicative of what will happen to called capital: For example, if a fund to which you committed 100.000€ has an early exit of 10.000€, they might retain that ‘distribution’ for later investment, meaning your total cash payable to them might just be 90.000€, or 90% of your commitment, or return that capital to you because they expect not to call it back (in full) prior to the end of the investment period.

For the sake of my analysis, I will not spend time considering Market Values. Practically, if we have a fund in our books at 5x but only model a 2x return, we might consider earmarking less capital as eventual distributions from that fund would positively affect our overall liquidity needs. However, I advise against being to precise in your models, as you risk building a model that is scheingenau (“seemingly accurate”): One in which you try to accurately model every single fund-level investment, which will end up producing the same results as a much simpler model as your overly precise assumptions deviate in both directions.

What other information do we need? First, some more detail on our funds:

Fund Type: We need to know if the fund is a VC, PE or secondaries fund, as that will have a substantial impact on our (expected) cash flow and return profile.

Vintage Year: We need to know in which year started investing, as that gives us an indication over which period the fund is allowed to call capital, and successively, over which time we’d expect them to return the invested capital as exits take place.

Second, we need to add our proverbial “x axis” to outline the variables of our existing funds investments above over time.

Called Capital over time: First, we need to know over what periods (i.e. months, quarters, years) the capital of existing funds was called. For example, if we committed 100.000€ to a fund in 2022 which has called 60.000€ so far, we’d want to know in what frequency that capital was called. Was it evenly spaced out over those three years, i.e. 20.000€ per year? Or did they start investing later but called more quickly? That information gives us an indication on how we’d expect future capital calls to be spaced out. (When in doubt just ask the fund on how the GP themself expects to call the capital.)

Distributions over time: Similar to our capital calls, it’s helpful to us to know what capital was distributed so far, and when during the fund lifetime: Was it during the investment period, when it might reduce our expected overall capital calls (as I had outlined above), or was it an exit outside the investment period, i.e. during the time of ‘harvesting’ profits?

If we put all of this information together, our overview becomes a little bit clearer:

Source: Cape May Wealth.

So now we know what happened in the past. But how should we think about (uncertain) future cash flows?

The Challenges of Single Fund-Level Data Modelling

In our chart above, we’ve outlined how a fund has done since our investment. For performance management purposes, that can be helpful, for example for a public-market equivalent (PME) calculation. But if we want to model our future liquidity needs, we need to make assumptions about how our fund investments - both existing ones and new ones, assuming you are planning on making new commitments - are expected to draw and distribute capital.

There are numerous ways to model fund-level cash flows:

You might think about private equity as an asset class generating excess returns over public equity. Fundamentally, that is true, and I find it to be useful for a fully established portfolio (i.e. if you want to think about long-term return expectations of private equity). But as with any ‘macro’-level analysis, it’s hard to model the short-term in more detail, i.e. how our individual funds drawdown capital.

You might take the ‘academic’ approach. Here, Yale University’s Takahashi-Alexander model is frequently mentioned, which tries to model cash flows and IRRs based on the so-called bow factor, which determines how quickly a given asset class is expected to distribute assets. While (in my view) simply enough to be used in a professional setting, I find the ‘bow’ factor somewhat unintuitive.

In the end, I think a model is best usable if it is practical and easily understandable. So if I want to build a model outlining cash flows at the level of a fund portfolio - why not make assumptions about a single fund’s cash flows?

Source: Cape May Wealth.

There are good arguments against modeling funds that way. You can certainly also model them more precisely, i.e. using quarterly or even monthly cash flows. But personally, I like this approach the best, and it has worked well for me so far. (Once again, no need to over-optimize to be scheingenau.)

But how do you get the cash flow data? It’s not easy! Funds are notoriously cautious with their performance figures, let alone their precise cash flows. I frequently get asked about the quality of some of the alternative investment databases - but without mentioning names here, I’ve been disappointed by most of them. In my view, they are either too expensive (think low five figures) for low-quality data, or they are extremely expensive for high-quality data. For the family office I work for, neither of these was an option.

So instead, I’ve tried to gather data directly from individual funds and different fund types, to build a data sample that is likely not representative but still sufficient enough for my purposes. Remember scheingenau: Perhaps there are some flaws in my assumptions around an individual fund, but if I make four fund investments per year over a 10-year period, it’s likely that positive and negative deviations offset any imprecision. (All models are wrong, but some are useful.)

My Assumptions (and reasons to disagree with them)

So what assumptions would I make for a private equity fund? Let’s fill in the blanks:

Source: Cape May Wealth. The figures above shouldn’t be taken as expected or guaranteed returns for a fund. They are solely for illustrative purposes. There is no guarantee that an investor will achieve such returns.

And in a bit more detail:

In terms of capital calls, I would expect the fund to draw 100% of the committed capital linearly over 5 years.

In terms of distributions, I would expect the fund to make the first distribution in year 5 (which will partially offset my last capital call), before then starting to distribute funds over time.

In terms of overall cash flow profile, I would expect net distributions (i.e. distributions minus capital calls) in year 6, and I would break even in year 7.

Overall, my hypothetical fund generates a MOIC of 1,7x, and an IRR of ~12%.

And clearly, there are a number of assumptions here:

There’s the overall timing of the cash flows, which practically can vary heavily even among private equity funds. Some might try to distribute money as early as they can (via dividend recaps or early exits), some might wait until the last second to sell their prized assets in year 9 or 10. I tried to depict what I would deem an average cash flow profile.

And embedded in that is our expected performance of a 1,7x net return. I could keep the same overall cash flow profile as outlined above, but might expect a higher return, which can be simply achieved by increasing the expected distribution in later years. Many investors, including me, aim higher in terms of return or speed of capital (but more on that below).

And lastly, I assume an average market environment. As private equity investors can see right now, distributions might ebb and flow depending on the exit environment, which can heavily influence your fund- and portfolio-level cash flow profile. (More on that when we go into the fund-level model.)

As frequent readers know, I tend to be more on the cautious side when it comes to tasks such as liquidity planning. You can also see that in my assumptions: One, the cash flow profile, where I expect that there is only marginal impact from early exits, and that 100% of the capital is called, both of which typically doesn’t happen for a private equity fund. And two, that my average fund achieves “only” a 1,7x multiple, when I am clearly aiming higher in my fund selection. Nevertheless, I see the benefit to being more realistic here, especially if you have invested in funds for a while and have a track record that would speak for higher performance figures and/or a better cash flow profile. But most investors that I help don’t have that track record just yet - and thus, I try to ebb on the side of caution.

So if you’ve stayed with me until here, and maybe even worked along with my instruction, you might be in a good spot. You should now have an overview for your existing funds, and should’ve made assumptions (or taken my figures) for an average fund, existing or new. Our next step now is to put it all together, and to take our model to better understand and optimize our cash flow requirements. But more on that next week.

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.