Welcome to this week’s edition of Cape May Wealth Weekly.. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive!

Welcome back to the newsletter! This and last week, we are tackling the art of capital call management: The field covering topics ranging from single-fund cash flow planning, to portfolio-level cash flow planning, and of course the best way to manage the required liquidity.

Last week on the newsletter, we covered single-fund cash flow planning, including not only what things to track but also assumptions on how we expect our fund to call and distribute capital. Today, we will take things to the portfolio level.

Building our Fund Portfolio Model

Last week, we ended our analysis by defining how we would expect an individual fund to perform - based on how they call and distribute capital. For an individual, average private equity fund, my assumptions were as follows:

Source: Cape May Wealth. The figures above shouldn’t be taken as expected or guaranteed returns for a fund. They are solely for illustrative purposes. There is no guarantee that an investor will achieve such returns.

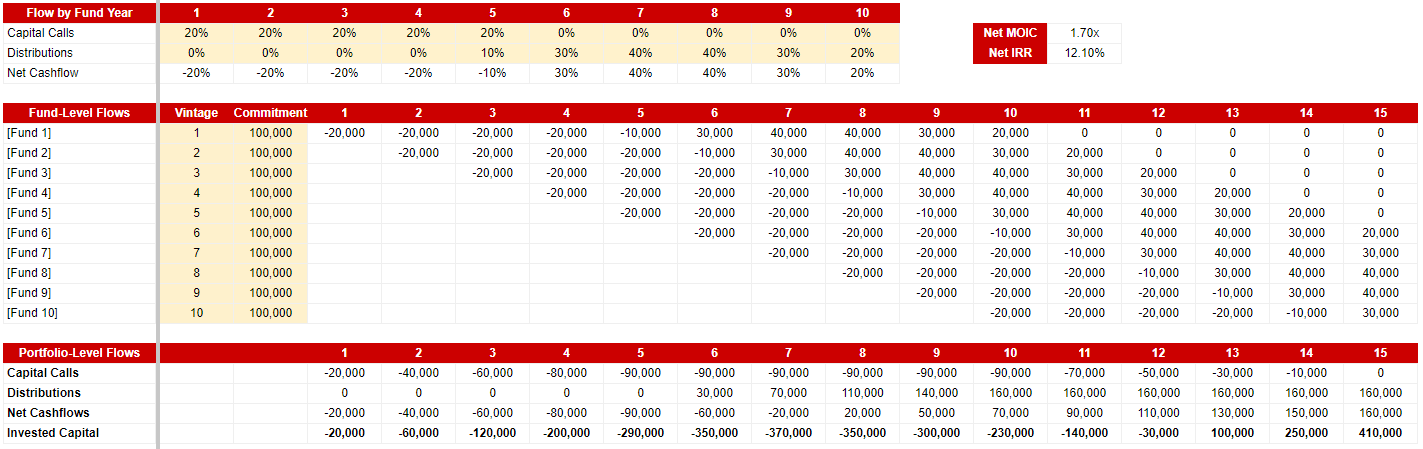

So that gives us an idea for an individual fund. For us to get a view of our portfolio-level cash flows, all we have to do is put things together:

Source: Cape May Wealth. The figures above shouldn’t be taken as expected or guaranteed returns for a fund. They are solely for illustrative purposes. There is no guarantee that an investor will achieve such returns.

There might be a lot to view here at first glance, but it is all surprisingly simple. Let’s go through from the top:

In the first block, you can see the aforementioned assumptions for our individual fund. 100% of capital is called until year 5, with distributions also starting in that year. We expect to see a return of our invested capital until break-even in year 7 / 8, and our fund will be fully liquidated by year 10:

Source: Cape May Wealth.

In the second block, we see the overview of our single-fund cash flows. Here, I assume that we commit 100.000€ per year over 10 years. Each line shows the individual performance of a fund, starting year by year. We can play with these figures as we wish - for example multiple funds in a year or different commitment amounts.

Source: Cape May Wealth.

And in the third block, we sum up our cash flows. We sum up our capital calls (how much capital do we have to invest?), our distributions (how much do we receive back), our net cash flows (the sum of capital calls and distributions in a given year), and lastly, our invested capital (how much have we in aggregate, over the different years, paid in or received from our fund portfolio).

Source: Cape May Wealth.

In our case, the third block might be the most insightful to us:

In Years 1 to 5, all we see is (net) capital calls. They increase steadily as we make new commitments, reaching its peak of 90.000€ per year from Year 5.

In Years 6 and 7, we start to see distributions. However, they don’t quite cover our capital calls just yet, meaning we continue to pay in (albeit smaller amounts).

Cash flow break-even is achieved in Year 8, when we have more distributions (110.000€) than capital calls (90.000€). This is a key milestone for any fund portfolio: You start benefiting from liquid returns in excess of what you pay in even as you keep on making new commitments. You are free to do with this excess cash flow as you like - you can re-invest it in the fund portfolio, you can invest it in other assets, or it might be the cash flow that you use to pay for private income requirements.

However, portfolio break-even is only achieved in Year 12, meaning that it takes us 12 years to receive our invested capital back. Only then do cash flows start to generate capital in excess of what we have paid in. (Of course, it is not until then that investors see a factual return on their capital - it would be in Year 12 where you are even on a cash basis, but you’d also still have a significant amount of capital in illiquid, yet value-retaining fund stakes.)

Which conclusions can we draw here, even with our generic model? For me, there is two:

First, that fund investments really are illiquid. According to my assumptions, a generic private equity fund would take until Year 6 to start returning capital and would reach break-even (i.e. having returned more capital than an investor paid in) in Year 7 or 8. If we use this data and assume a portfolio approach, both of those are pushed even further back. This data varies even more heavily depending on what type of funds you invest in: A Secondaries fund might achieve break-even more early, but a single venture capital fund is likely to take until Year 10 or longer to reach break-even. If you then take these assumptions to the portfolio level, investors might reasonably have to wait 15 (!) years just to receive their invested capital back. If you are dependent on any form of short-term liquidity, traditional closed-end funds are definitely not an asset class for you.

Second, but perhaps controversially, that they are a great way to generate long-term cash flows. While nobody I know would call private equity an income-oriented asset class, I find it to be a great long-term portfolio building block for that exact purpose. While its liquid counterpart, public equity, offers similar long-term returns, it is subject to significant volatility, thus exposing investors to the challenge of market timing. If they want to avoid it while also looking for some sort of cash flow, they either need to sell indiscriminately, which might mean they sell even when markets are down, or they need to add stability-oriented (and often lower-returning) building blocks to their portfolio.

As we will explore in a second, the cash flow profile of a fund portfolio can be altered drastically depending on our market environment. But in my experience, it is at least positively exposed to market timing considerations: Given that most of a GP’s compensation comes (or should come) from carry, they tend to make sure that they sell an asset at the highest price. They also try to sell as early as possible to avoid their carry being reduced by their hurdle rate. As a result, even in challenging markets, some companies in a well-diversified portfolio will be up for sale at a good price - which should hopefully generate a distribution in an established portfolio. Anecdotally, more than one family office has told me that even in challenging years like 2023 and 2024, their distributions from a mature fund portfolio still sufficiently covered their ongoing capital calls of newer funds. But it’s not exits from average companies (which struggle to be sold) - it’s typically from the highest-quality companies that still find buyers at attractive prices.

Stress Testing: When things don’t go as planned

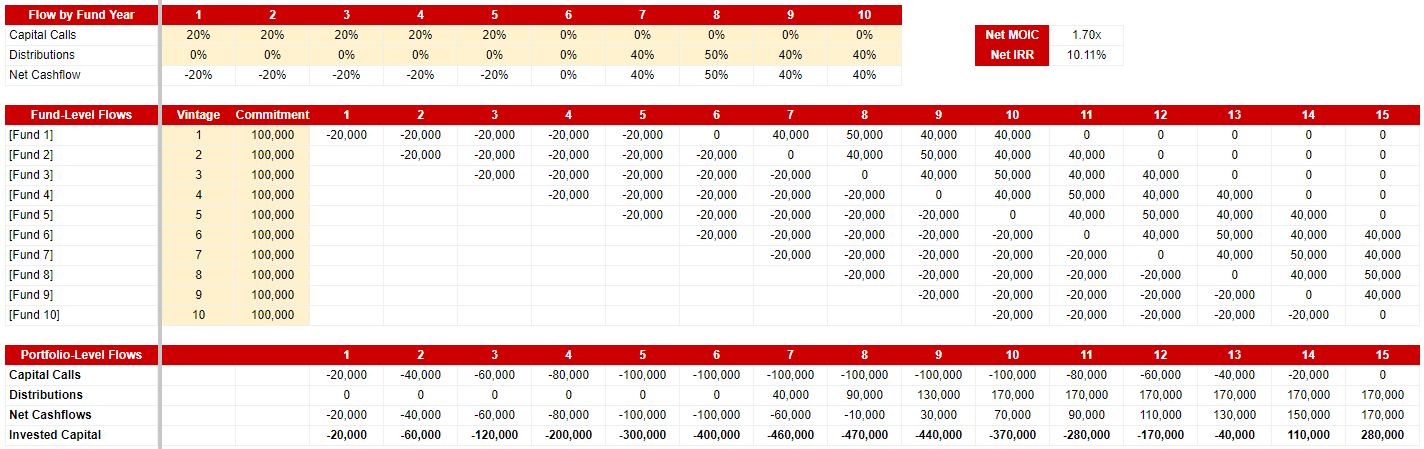

Assuming that everything goes as we see it in our model, we would expect our fund portfolio to reach cash-flow break-even after Year 7. Until then, we’d have to invest roughly half (370.000€) of our total outstanding commitments (700.000€). But what if we see challenging years, when distributions are scarce? We can - and should - model that as well.

What likely scenario models should we consider? The most common one, which I also find quite applicable to the current environment, is that each of our funds takes two years longer to distribute their capital. We don’t expect performance to be lower on a MOIC basis - we simply expect distributions to come later in the respective fund’s lifetime. (Our IRR would be lower, of course.)

Using our model, things would look as follows:

Source: Cape May Wealth.

With no distributions in Year 5 and 6, our net cash flow break-even moves back from Year 8 to Year 9. More importantly, however, is that our maximum invested capital increases notably from 370.000€ in our “Base Case” to 470.000€ in this scenario. As a result, portfolio-level break-even is also pushed back to Year 14.

Is that a likely scenario - that all funds, regardless of the economic scenario, take two years longer to distribute capital? In all honesty, likely not. Given that their annual hurdle rate works against their carry eligibility, GPs are always primed to distribute capital earlier rather than later. But we’ve also seen a shift in GPs holding onto winning assets longer, either in their fund or through Continuation Vehicles.

So why is that still a model to consider? Because it is a simple, yet meaningful risk management exercise. Investors should never forget that a 100.000€ commitment means that they are on the hook for that full amount - or in our case, the full 700.000€ being called until our break-even in year 7. Maybe our original figure of 370.000€ is too aggressive, and 470.000€ actually more of a realistic base case. What is more accurate? That is your choice. My instinct would likely to earmark something around 500.000€.

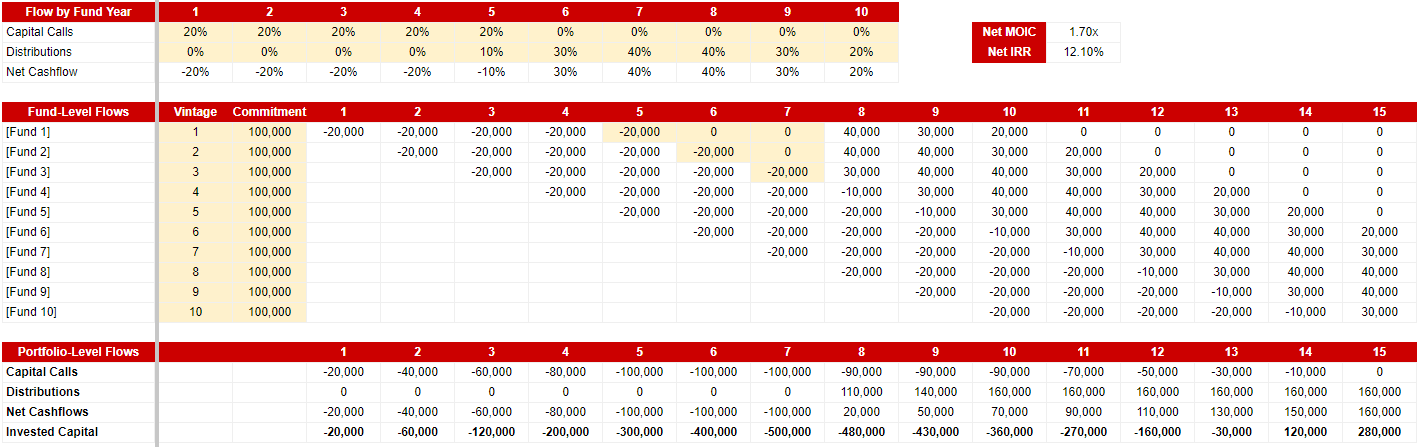

We can also consider an even more aggressive case. What if our early funds don’t distribute any money in their early years, just as we get to our ‘expected’ break-even in Years 5-7 - and they stay there, i.e. see their performance permanently impaired? While most experienced private equity investors tell me that it’s very unlikely to lose money on a fund, it’s not impossible. It certainly happened in especially challenging times such as the GFC, or might also happen if your early fund investments were with a truly terrible GP.

Let’s try to model that as well:

Source: Cape May Wealth.

Our case is the same, except that we expect that our first three funds will run into trouble just as we’d expect them to distribute cash. They see no distributions from Years 5 to 7, and stay impaired, meaning that Fund I even loses money. Here, the impact on our cash flow profile becomes even more severe: While we still expect break-even in Year 8, our total invested capital moves to 500.000€ out of 700.000€ in outstanding commitments until Year 7. Substantially higher than our first case, and conveniently in-line with my prior instinctive figure (without planning for it, I promise!).

The Case for Doomsday Scenarios

When a client of mine showed my (conservative) fund cash flow model to another advisor, they called it factually correct, but akin to a “Doomsday Scenario.” I understand that reaction - after all, there is a good chance that an investor will actually end up with better cash flows and better returns than what my model would expect. I might likely not be doing myself a favor when trying to sell a client on the asset class.

So why am I so conservative when it comes to liquidity planning? Because the stakes are fundamentally different for public and private equity. If you expect a 30% drawdown in your public market portfolio but incur a 50% drawdown, you hopefully will make the choice to simply not to sell. If you are not dependent on short-term liquidity from your portfolio, you hopefully just have to weather the storm until the market and your portfolio recover. For an illiquid portfolio, if you earmarked 370.000€ but have to wire 500.000€, it might be fatal: If you can’t come up with the liquidity, you might lose all of the capital you previously paid in, and might be still on the hook for the remainder.

In the end, I can only guide my clients to what I think is the right figure, using a more nuanced version of the model you’ve seen today. If we agree on this figure, we get to the last, but perhaps most discussed part of capital call management: Figuring out how to park the required liquidity. How do we go about that? More on that in the final part of our series, next week. Stay tuned!

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.