Welcome to this week’s edition of Cape May Wealth Weekly. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive!

Few things are as much-debated in the world of investing as the question of Market Timing.

Investors relying on technical analysis or quantitative investing frameworks swear that they know (at least, on average) one should enter or leave the market. Financial advisors say that there is no proof for market timing at all. Yet their clients (including mine) see the stories of Michael Burry or David Einhorn as proof that market timing could help them build a fortune.

So if you find yourself with liquidity looking to be invested in the market, how should you proceed? Let me tell you how I help clients approach the matter - and more importantly, what hidden risk many individuals underestimate as they think about how to enter the market, and why underestimating this risk might set them up for failure in achieving their long-term returns.

Why Care About Market Timing?

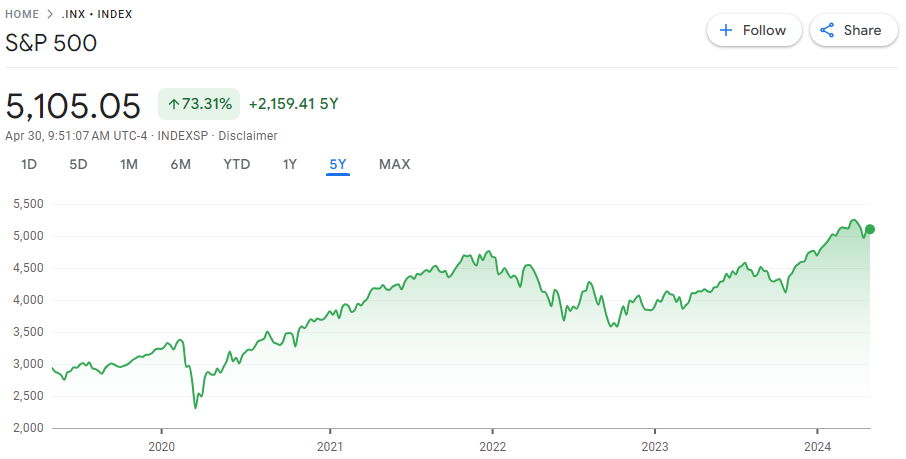

For those unfamiliar with the matter, Market Timing typically addresses the question of whether there are signals that help investors enter (i.e. invest in) or leave (i.e. sell out of) the market, thus optimizing their returns. It’s unsurprising that so many investors are obsessed with the matter. Take the S&P 500:

Source: Yahoo Finance (April 30, 2024). Please note that the above is an index excluding any transaction fees or product expenses. Historical returns are no guarantee for future performance.

Had an investor entered the market exactly five years ago (from when I write this article on April 30), they would’ve generated returns of over 70%. About a year into their investment, they would’ve seen a substantial drawdown in early 2020 amid the fears around the COVID-19 virus. But just imagine if you had seen the virus coming, and had sold out of your investment at the prior peak ($3380 on February 14), and bought back at the bottom ($2305 on March 20): You would’ve returned roughly 15% until selling out of the market, before generating another 120% from the market lows until today, but a total return of over 150%. More than double of our regular return - and that’s without taking into account that our return could be even higher as we could’ve re-entered the market with additional capital.

But as always, that is easier said than done. So let’s ask yourself the most important question: Can you actually time the market?

The Rational View

Frequent readers know that I am not a quantitative genius, Finance Ph.D. or similar. Nor do my clients typically have those qualifications (otherwise there’s a good chance they might not be my clients, and rather take care of their finances themselves!). Accordingly, my view of the market tries to be quantitatively informed and numbers-driven, but not dependent on large-scale statistical analysis.

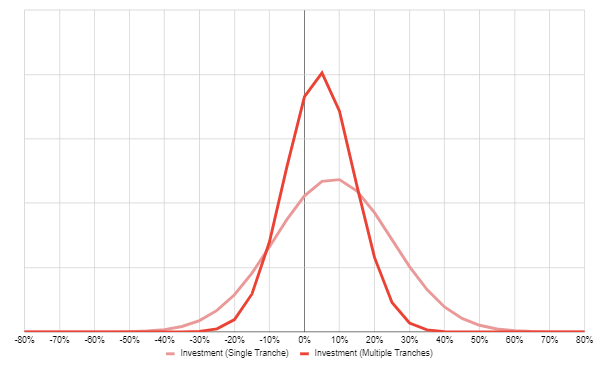

And I tried to conduct such a piece of quantitative analysis myself, comparing two scenarios: One, in which we invest all of our capital into MSCI World immediately (i.e. no tranching), and one, in which we split our investment into twelve equal tranches, each invested monthly over a period of 12 months. You can see the results below:

Based on MSCI World Net Total Return Index in USD since January 1970. The analysis below shows the historical return of two investments over a 12-month time period: One investment, in which all capital is invested in the first month of the 12-month period, whereas the other one is split into up to 12 monthly tranches. The analysis is based on historical returns. There is no guarantee that an investment will perform as demonstrated here. Historical performance is no indicator for future performance. This analysis does not reflect any transaction or product fees. In addition, the analysis does not include potential interest paid on uninvested capital. Investors that invest in EUR also need to take into account the impact of currency fluctuation.

To explain how you should read the chart: The above shows the two scenarios in a normal distribution, with the x-axis representing the potential returns and the y-axis demonstrating the frequency of such returns. Taking our Single-Tranche scenario, we can see an average 12-month return (i.e. the highest point in the curve) of roughly 8%, with 12-month returns ranging from almost -50% to over +60%. Our distribution for the Multi-Tranche is much more narrow, with an average 12-month return of just over 4% with 12-month returns between -36% and +35%. You can see the exact figures below:

These results should not be surprising, and feel instinctive on closer analysis: If we assume that the long-term average return is roughly 8%, it seems right that an investment split into 12 tranches (i.e. on average, 50% invested) would return 4% (excluding interest paid on cash in this analysis). Equally, it’s not surprising that the single-tranche investment has stronger outliers both in positive and negative scenarios.

So what conclusion should we draw from this - does market timing work, or not? In my view, it depends on what is important to you:

If you want to use market timing to maximize your return, then using the single-tranche logic might be the way to go. Picking a specific (or even random) single date offers, according to my analysis, the highest expected return, as well as the highest upside potential (if we compare the best return scenarios).

But if you want to minimize your potential downside, perhaps consider the multi-tranche approach. While your average return might be lower, your downside scenario was historically lower in the multi-tranche approach. Also, while not reflected in this analysis, your expected return benefits from the current environment of positive interest rates, allowing you to generate returns on your uninvested cash without market risk.

So finally, you might wonder: What is my preferred approach? Let me tell you what I think.

The Psychological Risks of Market Timing

As outlined above, any advice that I give to my clients should be based on data and quantitative analysis without being too complex. Once that analysis is complete, I try to draw conclusions that are aligned with a client’s individual needs and preferences - which might differ depending on their goals, i.e. if they are more focused on maximizing returns or minimizing risk.

Most of my clients tend to be return-oriented, even if they have some sort of risk preference in mind. Theoretically, I should advise them to invest everything in a single tranche, given that it offers the highest expected return as long as the worst-case scenario does not cause their portfolio as a whole to hit its risk limits.

But while the data might speak for it, do I advise clients to use the single-tranche logic? No, I don’t - for two reasons:

One, because my job as an advisor is to help a client optimize not their short-term return (i.e. the next twelve months), but their long-term return (i.e. multiple years). While the single-tranche logic might offer the highest short-term return, it also brings substantial risk of damaging their long-term return prospects. (Admittedly, that could be another piece of analysis that I still have to prepare.)

Two, and more importantly, because it bears substantial psychological risk - which is, in my view, the much bigger risk in getting your approach to market timing wrong.

Let me give you an example: A friend of mine had saved up a significant amount of money (for them) and asked me on how they should invest it. I shared with them the same analysis as the one above, and they opted for a significant upfront investment of about half of their investable capital.

And unfortunately, that happened to be at the end of 2021: Throughout 2022, they saw a significant drawdown on their investment, and thus, lost the motivation to invest more capital. They saw capital markets as a way to lose money over the short-term, not as an opportunity to build wealth over the long-term. And rather than invest the remaining capital throughout 2022, they stopped investing. Their initial investment has recovered and started generating returns, but they have since stayed away from additional steps into the world of investing.

And that, to me, showcases this big, hidden risk associated with getting market timing wrong:

That it permanently harms your view of how you should be investing in capital markets not to maximize short-term, but long-term returns.

So for those facing the question of when and how to enter the market, I would give the following advice:

First, before even thinking about when and how to enter the market, take your time to figure out what exactly you are looking to achieve. That includes topics such as your Investment Objectives, and as a result of that, your asset allocation and your preferred instruments to access individual asset classes.

Second, don’t feel pressured. Once people know you have investable capital, expect to be showered with countless opportunities that apparently you can and should not miss out on - yet you will find out that missing out on them often ends up being the better decision in hindsight. In other words: Don’t give into FOMO.

Third, take your time to slowly enter the market - even if it might make less sense rationally. To be clear: Except on very few occasions, I would always recommend my clients to at least intend to invest in multiple tranches, given the significant psychological impact of negative short-term performance. Accordingly, I would advise you to make a plan to enter the market over a period of time.

Take the example of a hypothetical client looking to reach their target public equity allocation by investing in equal tranches over a 6-month time period. As they start out investing, the market might either go down, or it might go up. In either of those scenarios, I tell them to try to see the positives: If the market goes up, they can be happy that they’ve already made some money, and to then invest more. If the market goes down, they can be happy to buy in cheaper with the additional tranches. And lastly, it’s important to remind them that deciding for a multi-tranche logic doesn’t mean that they lose their flexibility: If the market really falls significantly from one day to the other (think March 2020 during the initial COVID shock), there is nothing that would keep them from accelerating their investment, or if they are more skeptical, to slow down their investment pace.

Investors are especially keen to see returns just as they start out, which makes it especially important to remind them that they are investing for the long term. From my experience, investment behavior around market timing (including the aforementioned rush into certain asset classes, without making sure whether they fit a client’s long-term goals) are more likely to cause mistakes than to generate a substantial impact to long-term returns.

So while I see it as my responsibility as a financial advisor to maximize my clients’ returns, that can sometimes mean trading the potential of a short-term gain for (more) certainty of a long-term gain. Whether you are an advisor yourself, or investing your own capital: I advise you to do the same.

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.