Welcome to this week’s edition of Cape May Wealth Weekly.. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive!

In this series, we are addressing the rising trend of Permanent Capital: Investment vehicles that don’t have a fixed due date, such as a closed-end fund. In Part 1 of our series, we first explained the benefits and challenges of the closed-end fund models. We covered why GPs might be so interested in Permanent Capital. In Part 2 of our series, we gave an overview of different types of Permanent Capital - most importantly, the recent big trend of so-called Evergreen Vehicles (“EVs”). We explained some of their quirks and benefits, and I shared some of my personal preferences around what investors should look out for.

Today, in the final part of our series, we will try to figure out how EVs perform relative to traditional closed-end funds - using, as it should be, a structured quantitative approach. More on that below - including my analysis in Google Sheets for your own review.

What the GPs say

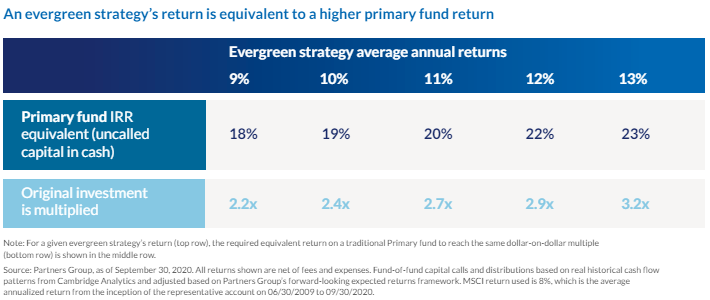

First, let’s see what GPs who are already active in the EV space say. Once again, we can take a look at an analysis by EV pioneer Partners Group:

Source: Partners Group.

According to their analysis, a traditional closed-end fund with an IRR of 18% should generate a multiple on invested capital of 2,2x. For an EV to achieve the same multiple, their average annual return ‘only’ needs to be 9%.

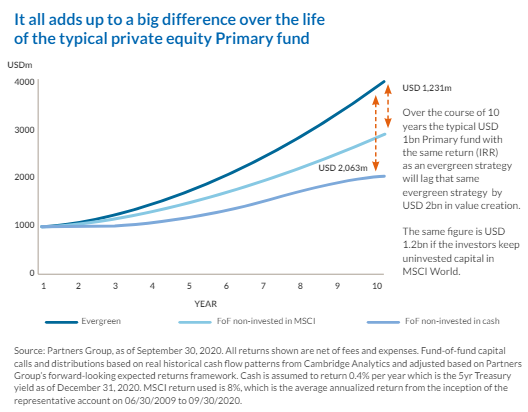

However, Partners Group goes even further and compares EVs with a closed-end fund over its entire lifetime, as well as a second scenario in which the closed-end fund’s uninvested cash is in the meantime invested in the MSCI World (assuming a 8% return p.a.). Once again, EVs seem to exceed its traditional closed-end counterpart:

Source: Partners Group.

I don’t know the returns of the EVs mentioned by Partners Group here. On first glance, the figures certainly look impressive. But we never want to be (potentially!) fooled by GPs - we want to make sure we understand their math to make sure that it withstands scrutiny. With that in mind, let’s try to evaluate, and ideally replicate, those figures.

Let’s start with the second graphic, where the numbers are a bit easier to assess: Without exact figures shown here, we can roughly estimate that $1BN invested in an EV grew into $4BN over a 10-year period. Using simple math, that would mean that Partners Group assumes a (4BN/1BN)^(1/10 Years)-1 = 14,9% net return per year - and not IRR, as private equity funds typically show, and almost 7% (!) excess return over their comparable MSCI return of 8%.

Frequent readers might remember the prior article on the Quantitative Approach to Private Equity, where we showed that 2nd/1st Quartile funds range between 12,5% and 18,9% per year, although each with shorter compounding periods, and thus, lower multiples over their term (2,0-2,7x vs. 4,0x for the EV). Hence, the numbers shown by Partners Group are definitely on the higher end.

What the numbers tell us

But let’s finally get into the analysis that you came for: A quantitative comparison between closed-end funds and evergreen vehicles.

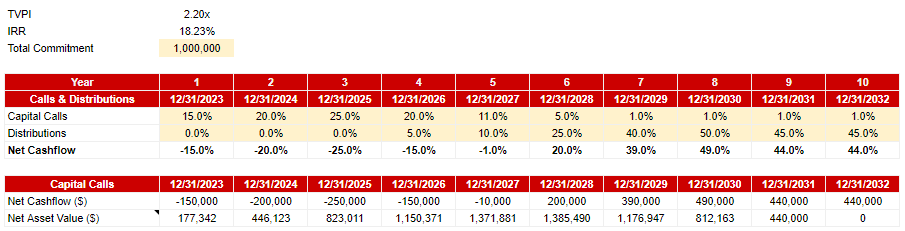

To start with that analysis, let’s first look at our closed-end fund. I am trying to show figures that match the numbers by Partners Group, which means I am assuming a somewhat ambitious performance: A TVPI of 2,2x over a 10-year holding period, resulting in an ~18% IRR. We try to fit the cashflows so that we get to our desired TVPI and IRR, which leads us to the following cash flows and NAV:

Source: Cape May Wealth. Please note that I forecasted the NAV on the basis of the IRR derived from the net cashflows above. Hence, the YOY increase in value in the NAV is equal to the NAV. In reality, it would not grow so linearly but likely be more in-line with the traditional J-Curve growth, in which NAV is first negative, then grows rapidly, and then stabilizes in later years of the fund. The numbers here are shown for illustrative purposes only and should not be used as reliable data for future private equity returns.

Those are typically the figures and KPIs that we see in private equity reports. But to make our numbers comparable to the EVs later, we need to translate them into time- and money-weighted returns. First, we do this for just the closed-end fund (excluding cash, meaning that capital calls come in as an external inflow, and distributions become external outflows):

Source: Cape May Wealth. The numbers here are shown for illustrative purposes only and should not be used as reliable data for future private equity returns.

While analytically correct, this is a deceptive calculation, which many new investors to private equity misunderstand: They see the yearly return identical to the IRR and assume it to be their money- and time-weighted return, and assume that it compounds to significant sums as outlined here (i.e. the 433% total return resulting in a 5.33x).

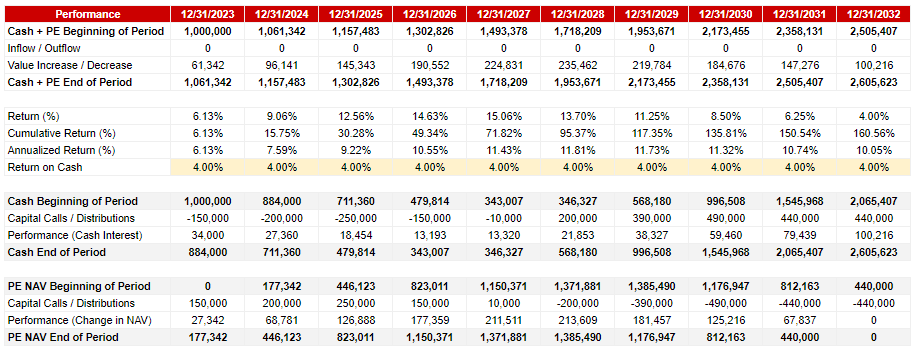

Analytically, that is correct - but only as long as you look at just that private equity fund individually. However, to do a proper time- and money-weighted performance analysis, you should also take the cash into account that is required to service those capital calls:

Source: Cape May Wealth. The numbers here are shown for illustrative purposes only and should not be used as reliable data for future private equity returns.

To help explain: At the top, we see our total annual market value for the sum of our earmarked cash and the PE fund’s NAV. We have a more detailed overview at the bottom - one for cash, where you can see outflows from cash for capital calls and inflows into cash from distributions, as well as the return on cash (here assuming 4% p.a. in line with current interest rate levels). Below, we have the PE NAV development, which as you might realize matches the stand-alone fund investment mentioned above.

When we add up these numbers, we see that we now get a blended return taking into account the cash required to fulfill our capital calls, and unsurprisingly, returns are significantly lower than our IRR (and the cash returns of the stand-alone fund), ending up at “just” ~10% p.a. over the full 10-year period.

And this ends up being a surprisingly anticlimatic answer to the question of what return an EV needs to generate to match the return of its closed-end equivalent: As we’ve made the conversion to time- and money-weighted return, we can come to the conclusion that our EV needs to match the total 10-year annualized return of the combination of cash and closed-end fund - so a required return of ~10% p.a.:

Source: Cape May Wealth. The numbers here are shown for illustrative purposes only and should not be used as reliable data for future private equity returns.

There are a number of conclusions to draw here:

The analysis highlights once again what significant differences exist between IRR and actual cash- and time-weighted returns. If your performance calculation includes not just the fund, but also the cash required to fulfill your capital commitments, your aggregate return comes down significantly.

The analysis shows the power of early, but continued, compounding. Most investors I speak to are interested in alternative asset classes for their attractive long-term returns, yet few consider how long it actually takes to get an alts portfolio fully up and running. If EVs can really start to compound from Day 1 of an investment, they don’t need excessive returns in order to match a well-performing closed-end fund.

EVs need to perform slightly better than Partners Group says. Assuming that cash generates interest until it is deployed, the return required for the EV to match PE + cash is 10% (rather than 9%). If we assume a higher return on uninvested capital (i.e. 50% at 4% interest and 50% invested in equities at 8% as they mentioned, i.e. a 6% blended return), the required EV return goes up another percent to >11% p.a. Admittedly, the difference might arise from cash flow timing (which they don’t share) and the assumed interest on cash (I use 4%, they use <1%).

And of course, it’s always important to highlight potential fallacies in my analysis:

We compare a singular, self-liquidating fund with a permanent EV. For a more realistic comparison, we should assume a portfolio of funds or a FoF - which would invest even more slowly initially, but would then compound at much more aggressive rates over time (esp. if excess cash results in higher subsequent commitments). Such a portfolio or FoF will hold less cash, and thus compound at rates that can come very close to the compound IRR - maybe not 18%, but 12-15%, and thus, ahead of the EV. As a result, over the long term, the portfolio of funds should catch up with the EV, and outperform it.

More importantly, we (and Partners Group) assume a somewhat ambitious performance. A 2,2x multiple for a PE fund, let alone a diversified portfolio of funds, is significantly above the average PE fund (which was historically closer to 1,7x). We shouldn’t forget that EVs make similar investments as a closed-end fund, but simply have more favorable liquidity and compounding mechanisms. However, these mechanisms don’t affect the underlying returns, but just their timing. Assuming more realistic returns of 1,8x TVPI for our underlying fund, the performance of the EV would be “just” 8% p.a. - still 1% ahead of the long-term equity return, but far from the figures we’ve seen Partners Group mention. If we take into account the current macro-driven difficulties that PE funds face, as well as the continued, increased competition in the market, it is reasonable to question whether future returns, whether for an EV or traditional fund structure, will live up to their historical returns.

Lastly, there are also many factors that our simplified analysis hasn’t covered, such as analyzing what investments EVs actually make relative to their closed-end funds, or assessing the impact of the different carry model (which is paid out annually, rather than upon a liquidity event, which negatively affects compounding).

Evergreen Vehicles: Is the hype justified?

In the end, you might wonder what my personal view is on EVs. As with other examples of ongoing financial innovation (such as Continuation Vehicles), my verdict is still out.

In terms of performance, it is simply too early to tell: While some players such as Partners Group have been in the market for a long time, many GPs are just now launching their first EVs, some of which I as a big nerd find intellectually interesting (such as Apollo’s Aligned Alternatives, or AAA). But especially as we go through challenging times in the market, in which even large GPs struggle to keep some of their companies afloat, I’m cautious to judge the performance of their newly-launched vehicles - I wouldn’t be surprised if GPs fill them with deals that they know will do well (see the recent press about Blackstone’s BREIT, which highlights the often-raised issue with how NAVs - which drive carry - are calculated), but at the same time, have a hard time judging them for not-so-great performance in a challenging market.

But if we can assume that the performance of private equity continues to show a reasonable outperformance over public equities, I think that EVs can be a game changer. Their structural benefits are significant:

For small investors, EVs make accessing private equity and other alts significantly easier - more than one client decided against it (or stopped investing in alts) given the challenges around liquidity management. EVs can be as simple as a one-off investment.

For institutional investors, EVs might make it significantly easier to ramp up an alts portfolio. My analysis might be purely theoretical, but based on what I’ve seen, it holds true: Investors can deploy significant amounts of capital more quickly than they could with closed-end funds (even with faster-deploying funds like secondary funds), thus getting to their target allocation earlier. In theory, flexibility around redemptions also allows for better rebalancing (perhaps outside of market turmoil).

For large investors, I don’t expect EVs to fully replace closed-end funds. As I outlined above. EVs have a cash drag component - so for investors that are long-term oriented and can also invest in closed-end funds, I would see EVs as a complementary solution, but not a full replacement. But maybe that isn’t even needed: All I want as an LP is another tool in my toolkit that better helps me deal with my challenges. If performance somewhat matches the closed-end funds, and their liquidity features work as intended, EVs can be a great addition to said toolkit.

Thank you for sticking with me through this series - as promised, please find my Google Sheet for your personal review here.

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.