Welcome to this week’s edition of Cape May Wealth Weekly. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive!

The Alternative Investment industry has seen tremendous growth over the recent years.

It might be because they have historically offered excess returns relative to its public market equivalents - although the question stands to what degree this excess return will persist in the future amid higher rates and increased competition. I’m cautiously optimistic.

It might be because of their lack of volatility. LPs only see quarterly NAVs, thus avoiding the impact of large mark-to-market swings and potential urges to panic-sell. But we are all well aware of how the quarterly marks, and ‘flexibility’ around pricing, can lead to less-than-realistic prices.

And admittedly, some of its rise might be fueled by a fee model that is very attractive to GPs.

Yet in the last few years, we are seeing a new trend emerge: The hunt for Permanent Capital. Vehicles related to this trend tend to offer lower fees, and more flexibility around liquidity, than Closed-End Funds. So why would GPs go in that direction? Some say it’s so that GPs can target clients that aren’t reachable with the Closed-End Fund model. Others say they are looking for a pool of capital for less-attractive assets.

I used to be critical as well. But the more I dig into the matter, the better I understand the appeal for GPs - and more importantly, the LP side. Let’s analyze the Rise of Permanent Capital.

The Benefits (and Challenges) of the Closed-End Fund Model

In the case of the widely-used “Closed-End Fund" model, investors entrust GPs with a certain amount of money (the “capital commitment”), which the GP can call over a 3-5 year period in tranches for investments and fees (“capital calls”). After 10-15 years, investors expect the GP to fully liquidate the fund and to return funds to the investors with a profit. In return, the GP receives an annual management fee, as well as a profit share (“carry”) on returns in excess of a preferred return for the LPs (the “hurdle rate”).

How does this differ from public funds? First of all, except in rare cases, LPs are required to fully pay in their committed capital. Subpar performance by the GP might affect their entitlement to carry, but not to the management fee. They can also not force the GP to provide liquidity prior to liquidation of the fund, so if LPs require early liquidity, they need to find someone to take over their Capital Commitment - which usually includes selling their stake at a discount to its net asset value.

Second, they differ by their fee model: In alternatives, fees are much higher than ETFs or mutual funds, ranging from 1% (private credit) to 2% (PE/VC). This fee may also be payable on committed capital, meaning that an LP might have to pay the full annual management fee even before their capital is fully invested.

Combining the 10-year term and the lock-up, it’s a great deal for GPs, with a decent-sized fund providing substantial management fees, regardless of actual success (and resulting carry payments). (Of course, the industry would’ve not reached its size if it wasn’t delivering sufficient returns to LPs.)

But of course, things aren’t perfect. Closed-End Funds are “self-liquidating”: They are split into an investment period (4-6 years), in which the GP can make new investments (excl. follow-ons) with the fund, and a holding period, in which all distributions need to go to the LPs rather than be reinvested. In addition, the management fee typically decreases after the investment period (and fully goes away at the end of the term).

At this point, GPs typically try to have a follow-on fund (with the prospect of a new, full management fee) ready. But in the current market environment, paired with increasing competition in the market, even large, institutionalized GPs are having a hard time raising capital for successor funds. In other cases, GPs might want to grow their firm, but don’t want to dilute their strategy through larger or more frequent funds.

There are a few ways for GPs to mitigate those Closed-End Fund-related issues. They can diversify their LP base by raising funds outside their own jurisdiction (take the continued attempts of GPs to tap into significant pools of capital in the Middle East). Or they can diversify their strategies, as we can see with GPs such as Blackstone or KKR becoming “one-stop shops” offering access to almost every type of alternative investment strategy.

But what if there was a model even better than the 10-year Closed-End Fund?

Longer-Duration Capital

The logical next step would be to simply increase the duration of your capital. After all, it’s what GPs want: Not only does it allow them to maintain their management fee streams, but it also allows them to hold on to good-predictable assets for longer - which in return reduces their reinvestment risk.

Surprisingly, the number of funds with a holding period longer than the usual 10+1+1 years is limited. While LPs might also be concerned about reinvestment risk, many prefer to have certainty in regards to when they can expect their capital back (even if that capital is invested into the same GP’s successor fund). Hence, longer-duration funds seem to be limited to asset classes that naturally match this longer holding period, such as GP Stakes or infrastructure funds. The only notably large long-term private equity fund that comes to mind is BlackRock’s Long Term Private Capital strategy.

The more popular way to keep assets and capital along for longer are so-called continuation vehicles (“CVs”). In the case of a CV transaction, GPs sell one or multiple assets from an existing, “end of life” fund (typically in years 7 to 10) to a CV. This CV is typically funded by an external manager (such as a secondary fund), which provides capital to buy out existing LPs that don’t want to roll over their stake into the CV and also acts as the third party pricing the transaction. However, they might also provide additional growth capital to the companies in the CV, for example for additional M&A or other strategic measures.

CVs seem like a good deal on paper: They allow GPs to hold onto well-performing assets for longer, while also offering LPs the choice between liquidity or reinvestment. They also allow GPs to grow or maintain their AUM without necessarily having to increase the size of their core funds. In practice, things are a bit more contested among LPs and GPs, with investors complaining about unfairly priced deals (as I recently wrote on LinkedIn) and PE critics stating that CVs are just another way for GPs to reshuffle assets without ever having to realize real liquidity in a market transaction.

More importantly, however, is that CVs are just an extension, but no alternative, to the Closed-End Fund model. For a CV to work, they still need to raise the fund from which a potential CV might one day emerge - which of course also requires fundraising.

So what if capital wasn’t just longer in duration - but permanent?

Why Permanent Capital?

The CFA Institute calls Permanent Capital the “Holy Grail of Private Markets.”

Permanent Capital, in itself, isn’t technically new: Balance sheet Permanent Capital has essentially been around since the beginning of capitalism, and its most famous contender, Berkshire Hathaway, has been around for more than 50 years. Some publicly-listed, Closed-End PE funds, have been trading in the UK for more than 25 years. So why is Permanent Capital only trending (again) now?

It has a lot to do with the evolution of private equity - and ironically, their return to public markets: As outlined above, GPs receive substantial ongoing revenues from their management fee. Another, and equally significant part, is carry, i.e. their share of a fund’s profits generated through its investments. However, carry depends on exits and their proceeds, which can vary substantially in timing and amount depending on the economic climate (as distribution-starved LPs can experience first-hand these days.)

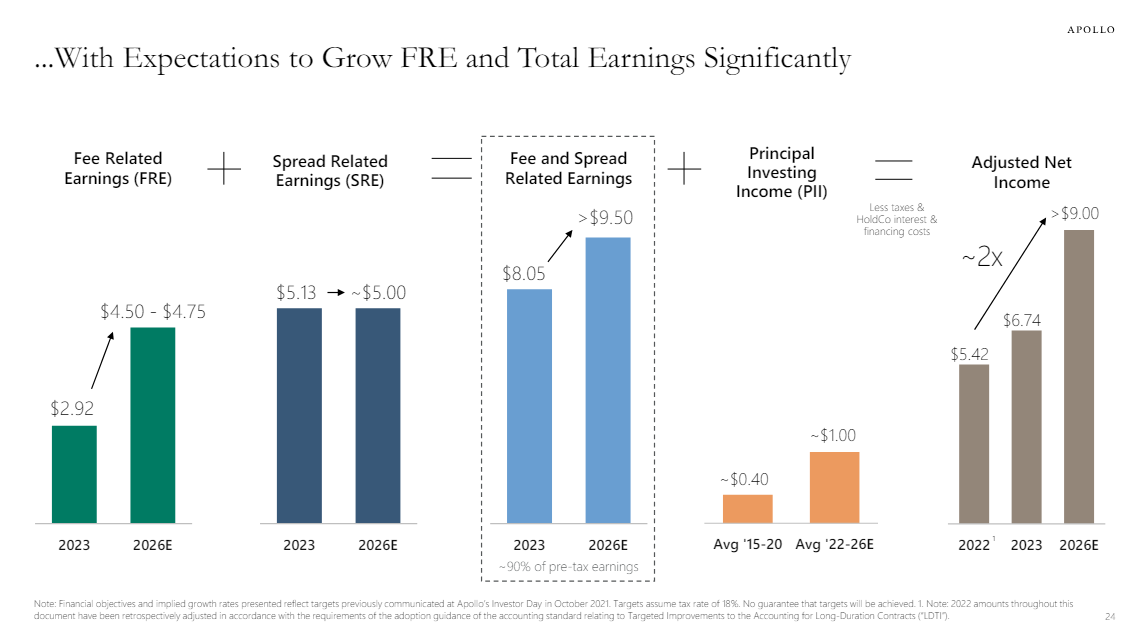

For a privately-held alternative investment firm, that is not a problem, as long as the management fee pays the bills. For publicly-listed alternative investment firms, things are different: Public market investors love predictability (like management fees on a 10-year fund) and dislike uncertainty (like a carry payment that may or may not crystalize). Unsurprisingly, research analysts value alternative investment firms on a multiple of fee-related earnings (“FRE”), and in return, those firms are working hard to find and grow their sources of FRE to grow their share price. Hence, GPs highlight to their investors how they look to grow their FRE…

Source: Apollo Global Management Investor Presentation (March 2024).

… or they might even go as far as buying rights to the FRE of other GPs, which has even evolved into a sub-asset class in itself, so-called GP Stakes Investing.

So now we understand why GPs care about Permanent Capital. But what does Permanent Capital look like in practice? Where does it occur in financial markets - and how should LPs think about this trend?

More on that in next week’s edition of Cape May Wealth Weekly.

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.