Welcome to this week’s edition of Cape May Wealth Weekly. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive!

DISCLAIMER: Throughout this article, I am mentioning a number of GPs and publicly traded closed-end funds to better give readers an example of the vehicles at play. Please note that mentioning those vehicles or GPs is for purely illustrative purposes. The mentioning of a specific fund or GP should not be seen as investment advice.

In this series, we are addressing the rising trend of Permanent Capital: Investment vehicles that don’t have a fixed due date, such as a closed-end fund. Last week in Part 1 of our series, we first explained the benefits and challenges of the closed-end fund models. We then discussed some longer-duration extensions of this model, including the rising trend of continuation vehicles (“CVs”). Finally, we outlined why GPs might be so interested in Permanent Capital: Because they offer them a more sticky, predictable revenue stream which helps them grow their fee-related earnings (FRE), a key metric for publicly traded alternative investment firms.

With that in mind, let’s tackle two questions some of you have already raised: First, what type of Permanent Capital are there - and second, what LPs should consider when thinking about Permanent Capital vehicles as an addition to their “LP Toolbox.”

“Traditional” Sources of Permanent Capital

Let’s begin with two sources of Permanent Capital that have been around for a while: Balance Sheet Funding and Traded Closed-End Funds.

Balance Sheet Funding is the most straightforward source of Permanent Capital. Rather than raising external capital, GPs simply make investments off of their balance sheet with cash at hand. While firms such as Blackstone or KKR have been more active in investing from their balance sheets in recent years, especially after they went public, this “direct PE” approach is not new at all - the most famous example likely being Berkshire Hathaway.

In some cases, GPs are required to make balance sheet investments, for example for their GP commitment to a new fund. In other cases, balance sheet investments might be more strategic, for example investing in assets that don’t warrant their own fund yet but in which they want to build a track record, or that might simply be a long-term investment beneficial to the GP.

The other “traditional” sources of Permanent Capital are traded Closed-End Funds (“CEFs”). For those unaware, CEFs, unlike open-ended funds (like a mutual fund or ETF), go public with a fixed number of shares outstanding that cannot be redeemed unless they are bought back by the fund, meaning that sellers have to find a secondary buyer. Unlike “private” CEFs, they tend to have no fixed term, meaning that they are quite close to actual permanent capital. GPs active with CEFs include but are not limited to HgCapital (with HgCapital Trust) or Apax Partners (with Apax Global Alpha). However, the most famous traded Closed-End Fund is probably Bill Ackman’s Pershing Square Holdings.

While the universe of CEFs is broad, they are somewhat limited in size and liquidity, and have thus seen few new entrants. They have instead been replaced by the most trending form of Permanent Capital: Evergreen Vehicles.

Evergreen Vehicles - the next big thing in alternatives investing?

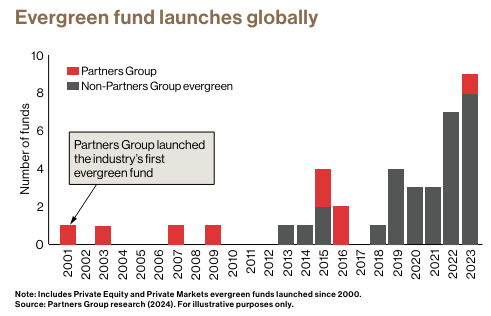

Judging by recent private equity conferences that I attended, Evergreen Vehicles (“EVs”) seem to be one of the major, trending topics in the alternative investment industry. Once again, they are not necessarily new: Swiss GP Partners Group set up its first EV in 2001, and was the lone pioneer (by their own assessment) in this niche until 2013. The more recent pushes into the markets are driven by a variety of factors, including but not limited to the new ELTIF regulations in Europe and/or the continued push of GPs to raise funds from private, affluent individuals.

EVs are structurally similar to a typical liquid fund (i.e. a public equities mutual fund). Investors can subscribe to the fund and receive a certain number of shares, based on their target investment divided by the fund’s current price per share (typically based on the fund’s net asset value, or NAV). Given that the underlying investments are not liquid, EVs don’t offer daily liquidity, but instead allow investors to redeem those shares after a minimum holding period and with some restrictions at fund level (more on that below).

In theory, the combination of a more liquid structure and the traditional alternative investment opportunity set allows for a powerful combination that in theory offers benefits to both GPs and LPs:

Institutional LPs, including family offices, that are invested (or are looking to invest) in alternative assets can more easily and quickly gain exposure to those markets. But they can also more flexibly adjust their exposure, for example in downturns that have historically caused institutional investors to be overallocated to illiquid assets.

Affluent investors receive easier, diversified access to alternative assets, similar to how a traditional fund of funds would give them, but can also avoid the headaches regarding liquidity management. They can also exit the asset class more quickly, if needed.

GPs can add another type of capital to their overall funding mix. While LPs can still ask for their money back (as was the case, for example, with Blackstone’s BREIT in late 2022), capital of long-term oriented LPs and the resulting management fee streams tend to be sticky in absence of scandals or subpar performance.

GPs gain a source of funding without a forced liquidation mechanism. They can theoretically hold well-performing assets for an unlimited time period, helping them mitigate reinvestment risk even better than the continuation vehicles we discussed in Part 1 of the series.

As often the case, those things sound good - on paper. But how do they look like in reality? In my view, in order to get a proper answer to this question, we need to consider three parameters:

Strategy: What does the EV invest in? Does it do direct investments, fund investments, or both? How much cash does the vehicle retain for capital calls and expected redemptions?

Performance: What is the expected performance relative to comparable investments (direct investment, fund investment, FoF)? How does the cash reserve affect performance at the fund level?

Liquidity: Do EVs allow us to invest in alternatives more quickly than a closed-end fund? Can I redeem my shares as freely as EVs promise?

Let’s try to answer all three of those questions, and let’s also try to highlight what I personally look out for in such products.

Strategy

Strategies used by Private Equity-focused EVs, to the most part, are not particularly different from closed-end vehicles in the market. They typically (co)invest directly into direct investments together with their funds, invest in their own funds as an LP would, or combine both those factors together.

Beyond that, the exact strategy seems to be dependent on who they are targeting: For products that continue to be focused at institutional investors, the strategy either tends to be focused (i.e. a private equity co-investment EV) or to be slightly broader over an asset class (i.e. a private equity EV investing into small- and large-cap funds as well as co-investments).

For products that try to tap into retail and affluent investors, I’ve also seen a broader strategy set. For example, one fund that I recently saw invests across real estate, private equity, growth equity and venture capital.

Personally, I would advise to always focus on the former type of product: If done right, they allow them to pick the best EV for a certain part of their portfolio (i.e. private equity, infrastructure, private credit) across a growing number of GPs offering EVs. For broader strategies, I see the real risk of a GP using it to invest into each strategy they have - and even with the best GPs, it’s unlikely that all of their strategies are worth their money. LPs might be better off with a “mix and match” approach.

Performance

Performance is likely the key point for anyone investing in alternative assets. In the case of closed-end funds, some investors might decide against an investment given the complexity and long lock-up, even if they offer higher performance. So how about EVs?

The gross performance of an EV fund making the same investments as a closed-end fund should not be fundamentally different from said closed-end fund. Beyond that, key differences arise, as always, from a difference in the level (i.e. absolute size) of ongoing and performance-based fees. However, there are two key differences: The handling of carry, and the so-called cash drag.

First, the carry. When I first wrote about Permanent Capital on LinkedIn last year, one reader asked how carry was handled, given that the EV might never sell out of an asset (which is typically the time at which a PE GP receives their carry). From what I’ve seen, performance fees are handled similar to how they would be at a liquid vehicle: Over a given period (i.e. one calendar year), the fund calculates its NAV-based performance. Once the NAV achieves a return in excess of its hurdle rate, the fund starts accruing carry, which is handled as a liability at the fund level, and is then paid out at the end of the year. We typically also see “high watermarks”, meaning that a fund manager doesn’t receive carry if the fund is below its all-time high (for which it has previously received carry).

As always, investors should be mindful of how the fee is calculated - especially for volatile assets, carry might be paid out at times unfavorable to investors (one example that comes to mind is UK closed-end fund Chrysalis, whose manager receives “eyewatering” performance fees on its Klarna investment when it was valued at over $40BN, and then came crashing back down).

Second, the so-called cash drag. Many GPs advertise their EVs with the statement that unlike closed-end funds, where investors take 3 to 5 years to be fully invested at the fund level, EVs offer investors the ability to be fully invested over 3-12 months or sometimes even immediately upon subscription.

However, in doing so, GPs (sometimes purposely) omit the fact that while investors might be immediately invested in the EV, that doesn’t mean that the EV itself is fully invested. After all, it takes five to seven years to fully invest a fund portfolio and to reach the portfolio “break-even”. And in the case of EVs, that doesn’t even take into account factors such as additional liquidity inflows from new investors that need to be invested as well, liquidity reserves for capital call management until the EV reaches break-even, and of course, liquidity buffers for investors looking to redeem their shares.

As a whole, these buffers can be significant. In the case of the two previously mentioned UK closed-end funds, Apax Global Alpha and HgCapital Trust, the liquidity (as of their latest reporting date) was roughly 6% (for Apax, as of March 31st, 2024) and 12% (for Hg, as of March 31st, 2024) respectively. Logically, given the lower expected returns on cash than a PE invested, this “cash drag” can reduce returns relative to a closed-end portfolio.

Liquidity

And lastly, an equally important question: Do EVs allow us to invest more quickly into alternative investments than closed end funds - and can I really get my money back when I want it?

On the first question, I am cautiously optimistic - keeping in mind, of course, the prior caveats around larger cash buffers (now at the fund level instead of at your personal asset allocation level) and the potential to have invested in an EV that itself is not yet fully deployed. However, most products that I have seen offer the ability to invest somewhat quickly (i.e. between imminent deployment on a monthly basis and/or deployment over 6-12 months). Accordingly, investors should rather ask themselves if they want to invest into just one or multiple EVs, and/or if they also stagger their investment similar to how a fund or fund of funds would do it - but that question is a science in itself.

The bigger risk - at least judging by media coverage - is around redemptions. First of all, liquidity is typically not available immediately after subscribing to a fund, with investors instead being subject to a lock-up of 18 to 36 months, or sometimes, an early redemption fee in said period. Beyond that, EVs are typically subject to so-called ‘gates’ at the fund level, which limit how much of the fund’s NAV or shares can be redeemed in a given quarter (typically 5 to 10% of total NAV). Lastly, GPs might have special rights to halt redemptions if they deem it to be in the best interest of the LPs, i.e. during a sudden market drawdown.

And we can see exactly that happening right now in two of the largest private real estate EVs: Property manager Starwood is allegedly running low on liquidity amid increased investor redemptions, having even tapped into most of its credit line. Blackstone’s BREIT faced similar challenges early last year, even tapping the University of California for a 4.5BN (!) investment with a guaranteed double-digit return as it was struggling with outflows (which however seem to have since subsided).

Personally, I am a bit skeptical on whether I should be concerned about GPs limiting outflows in times of market turmoil. I am not a real estate expert at all, but in hindsight, not selling out of real estate when interest rates peaked to fulfill investor redemptions might’ve been a good move for Blackstone and their LPs. Nevertheless, limited liquidity can be a challenge, especially if investors chose to invest in EVs exactly to have a liquidity option when their closed-end funds see fewer exits and thus no liquidity. In the end, alternative investments, even if they offer better liquidity, are a long-term investment, and investors should not think about being able to sell out of them in difficult times - just how they shouldn’t sell out of their long-term-oriented public equity ETF in a market drawdown.

You might wonder why we haven’t talked about exact performance figures yet. We will get to that - but it warrants, as usual, a more quantitative analysis. More on that in Part 3, and the final part of our Permanent Capital series.

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.