Welcome to this week’s edition of Cape May Wealth Weekly.. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive!

Many of the clients that we work with have a high degree of risk tolerance. They invest in higher-risk, higher-reward asset classes, whether that is a simple allocation to public equity or something more complex such as direct investments into early-stage start-ups. The presence of such riskier investments is no surprise, given that most of those clients made their money as entrepreneurs - without a doubt also a more risky path to building wealth.

However, in the end, many of such client portfolios consist of only higher-risk, higher-reward asset classes. When asking clients to explain their thinking, they typically argue that it’s based on the long-term expected returns of said asset classes. Take public equity: The asset class has historically offered highly attractive returns to long-term investors. But of course, those returns come at a price - among the liquid asset classes (excluding crypto given the short track record), it has demonstrated the highest volatility and drawdowns in times of market turmoil.

If you are solely a long-term investor investing into public equities planning to not touch your investment for the next twenty or fifty years, those risk considerations might be less relevant for you. Volatility might cause substantial swings in your portfolio value, but hopefully, you will benefit from the long-term average returns we’ve been able to observe over the last decades.

But more often than not, in the world of affluent investors, they don’t plan to just leave their investment for the foreseeable future. They might want to re-allocate to other asset classes over time, or they might need to sell assets to fund their lifestyle.

And if that’s the case, investors should be mindful of so-called path dependence. Let's explain what path dependence is, practical examples of the resulting risks in action, and lastly, ways to mitigate it.

What is Path Dependence?

Path Dependence Risk is the risk of an investor not achieving their respective investment goal due to non-linearity of the parameters that affect them. Admittedly it’s a bit of a clunky definition, so let’s break it down:

Investment goals can be both major or minor goals. Major goals would be what I often refer to als Investment Objectives - the high-level goal you want to achieve as an investor, for example a certain target return, an income goal or a maximum drawdown. Minor goals, in return, are the often numerous small tasks that together amount to investment success, for example being able to service the capital calls of your fund portfolio, which in return is one of the many pieces that make up your asset allocation, or having the cash available to pay an outstanding bill.

Parameters mean the measurable input factors on which our respective goal depends. The most common parameters that investors think of is typically return, i.e. the performance of an individual investment. Investors might also view return in the context of the invested capital, where more capital invested in a certain asset might necessitate a lower return or vice-versa. But an equally relevant parameter is also the other side of the equation, meaning how the invested capital and/or the achieved dollar return is spent. That might include outflows from the portfolio as a whole, for example for living expenses of the investor, or a reallocation of funds within the portfolio, for example when a fund in the fund portfolio is calling capital.

Lastly, and perhaps the hardest to explain with words alone, non-linearity. To explain it, let’s use my example from the introduction: That many affluent investors allocate a significant portion of their liquid assets to public equities, as it offers the highest average long-term return.

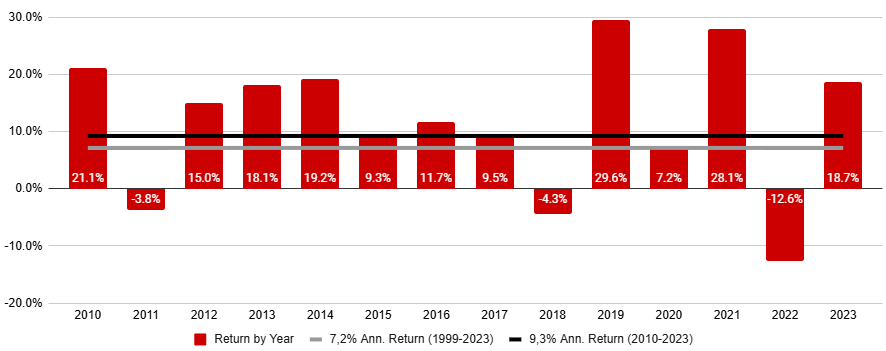

On the basis of average returns, that approach is logically sound. If we look at the globally diversified MSCI ACWI Index, we can see that it generated an average gross return of 7,2% p.a. since 1999. But we can also see non-linearity in action: In the period since 2010, the index only saw one year in which it actually generated a 7,2% calendar-year return (in 2020). In all other years, performance was either significantly above that figure (peaking at 29,6% in 2019), or significantly below (at -12,6% in 2022):

Source: MSCI, Cape May Wealth. Performance in EUR, before costs. Historical returns are no indicator of future performance.

Hence, as the name says - despite stability of long-term, annualized returns, calendar-year returns are non-linear. They fluctuate significantly from year to year, which might have a significant impact on how an investor might (or might not) achieve their goals. (More on that below.)

The same applies to the spending side. While most investors try to stay within a budget they set for themselves, there is always the risk of an unforeseen, extraordinarily large expense outside of what they had accounted for. Within investment portfolios, a common non-linear parameter is the cash flow profile of a fund portfolio, often fluctuating both for the benefit of the investor (i.e. lower than expected capital calls and/or larger distributions) or against them.

But why exactly is non-linearity such an issue? Let’s dive into a real-world example.

Example #1: Income-Oriented Portfolios

Assume that you are an income-oriented investor. You start with a portfolio of 10.000€ invested in an MSCI ACWI index fund, and want to make a (admittedly large) withdrawal of 700€ at the end of each calendar year, in line with the (expected) long-term return of the MSCI ACWI.

Let’s take a look at our definition of path dependence risk again: Our investment goal is to be able to withdraw 700€ a year from our portfolio, ideally without taking the risk of depleting the invested capital. There’s multiple parameters: There is how much capital we are investing (10.000€), how much we want to withdraw every year (700€), and most importantly, the non-linear parameter of return. This non-linearity is once again visible in the chart above: While we expect the long-term average return of 7,2%, our returns actually fluctuate significantly - and thus, our overall outcome might differ depending on when we start.

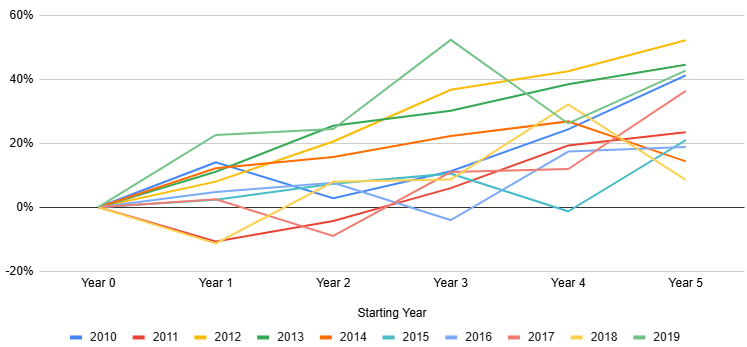

If we invest over a 5-year period, having started in any of the ten full 5-year periods since 2010 (i.e. between 2010 and 2019), we can see how non-linearity affects our overall outcome:

Source: MSCI, Cape May Wealth. Performance in EUR, before costs. Historical returns are no indicator of future performance.

Admittedly, it was a good period for stocks, so the outcomes are all positive - but they still vary significantly: Our best period (from 2012 to 2017) saw a return of +52%, while our worst period (from 2018 to 2022) saw a return of ‘just’ +9%.

For longer-term returns, we can take a look at Vanguard’s famous Return Handbook to see non-linearity in action: For all 20-year holding periods between 1901 and 2020, our average return was 7,5% p.a., close to the average return over the full period of 7,3% p.a.

But depending on when you started, the outcome might look substantially different. You might be lucky and get the best 20-year return, standing at a stunning return of 17,2% p.a. Or you might be unlucky and get the worst 20-year return of a meager 2,9% p.a. If you combine that with an income requirement, even a drawdown as small as 1% of your portfolio per year, you might’ve ended that 20-year period with your portfolio either substantially ‘in the green’, or standing at just a fraction of your initial capital.

Example #2: Derivatives

Affluent investors tend to use derivatives in a short-term, tactical manner, meaning that they want to use them to enhance their return through a directional trade. That might be a trade looking to benefit from the positive development of an underlying, for example the purchase of a call option on a single stock. But it could also be the opposite, for example the purchase of an index put option as a way to hedge a client’s overall portfolio.

And this short-term, tactical usage is exactly what makes those derivatives extremely path dependent. The two key parameters of an option, strike price and maturity, are substantial drivers of the gain that an investor might incur. To make this more concrete:

An investor might be right in their assessment of a stock and its long-term trend. But if the option they’ve chosen matures before their thesis plays out correctly, they might not benefit from the stock’s positive performance, and had to pay the option premium. The same goes with the strike price: Once again, an investor might have the right thesis, but factors outside the stock’s performance (i.e. a temporary market drawdown) might result in the stock not hitting its strike price prior to the option’s expiry.

As a practical example: In my personal account, I had bought some short-dated call options on the VIX (a volatility index often used as an indicator of perceived market risk) this summer when the VIX was on the lower end of its long-term range. On a Monday not two weeks later, we saw a massive spike in the VIX amid turmoil in the Japanese markets. But did I profit? Unfortunately not - my option had expired on the Friday before.

Hedging Against Path Dependence

So how can we protect ourselves from the risks associated with path dependence when using derivatives or in the case of an income-oriented portfolio?

As with other types of risks, we can benefit from the ‘free lunch’ of diversification. Let’s use the example of our income-oriented portfolio again: If we are invested entirely in equities, we might hit a winning period in which our returns outpace the amount that we need to withdraw every year, but equally, we might hit a period in which our portfolio returns become (further) negative due to our ongoing need for income. Here, diversification typically pays off: While diversifying away from higher-returning asset classes such as public equities might result in a lower expected return, we might also see a lower expected drawdown. More practically, even in a year that is bad for equities, we might have other portfolio components such as fixed income or commodities that see less of a drawdown or might even show a positive return - and as a result, we can sell such assets off at a gain or atleast a smaller loss to cover our expenses, while being able to ideally hold onto our risk assets such as equities until they recover from their drawdown.

For someone just starting to invest, we should also be mindful of market timing. In a prior article, I had shared that if we go by average returns, we’d actually be better off investing all of our capital in a single tranche rather than breaking it down into individual tranches. After all, being fully invested on Day 1 would mean that we benefit more from the long-term, on average positive return of the (equity) market. (Please highlight that I would advise against investing everything in one tranche despite the mathematical truth - more on that in the article.)

But of course, that comes at a price. Less tranches means that we are fully exposed to a single 12-month path, and are thus subject to a worse 12-month outcome. Staggering our investment into multiple tranches effectively breaks the number of ‘paths’ from one into multiple paths (admittedly with overlap). Hence, despite the lower expected return, we also see better worst-case outcomes, reducing the loss in the worst scenario from -48% to ‘just’ -36%. And of course, that is the case for an all-equity

Despite the lower expected return, multiple tranches reduce our worst outcome by ~12% (from -48% to -36%) and thus a more bearable level. And of course, that is for an all-equity investment. Imagine a diversified portfolio, invested over time - we not only benefit from the different paths underlying different asset classes, but also from different paths from different starting points.

And lastly, to touch on the challenges associated with our derivatives example: Consider whether they make sense not as a tactical, but a systematic investment.

If you purchase put options for your portfolio whenever you think that the market is overvalued, there is a good chance that you’ll do so when many other investors feel the same as you, making ‘insurance’ more expensive than usual while also facing the risk of missing the correct time for your protection trade.

But what if you try to think of ways to systematically - i.e., on an ongoing basis - include them into your portfolio? Take my co-founder Markus, who developed a clever way of systematically (and not tactically) using call options in some of our client portfolios to retain some of the public equity upside without being exposed to the full downside. I also know of some family offices who use substantial leverage ‘hedged’ through put options which they finance through the higher expected return of their leveraged portfolio. Both of those strategies can pay off - but they only work if you stick to them, especially when they seem to not pay off. I know of more than one story where investors gave up on their systematic hedging strategies just weeks before a crash (and substantial payday).

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.