Welcome to this week’s edition of Cape May Wealth Weekly. If you’re new here, subscribe to ensure you receive my next piece in your inbox. If you want to read more of my posts, check out my archive!

Any good investor knows that you can’t make money without taking risks..

With the exception of bank accounts with deposit insurance, and maybe some government bonds, investors have no definite certainty of a positive (nominal) return. They have to take risks of different scope and type, in hopes of being rewarded with a positive return on their invested capital. The bigger the risk, the bigger the potential return - but also the downside.

Most investors try to reflect this balance of risk in return in how they invest. This is typically done through traditional, portfolio-level risk metrics, such as maximum drawdown or volatility. But to my surprise, this is often where thinking about risk ends: Investors prefer to think about how to maximize their returns, even if they might not even be dependent on outsized performance. Time is spent on upside optimization rather than downside protection.

I would greatly recommend that investors take time to think about the risks they face. Not only does such an exercise in likely and unlikely risk, and their expected consequence, help you shape your mind and be prepared for unfortunate events.

But it is also because knowing the risk you face opens up a whole set of possibilities: To choose which risks you want to take, and which not - and how to deal with those you can’t avoid.

Defining Risk

Fundamentally, I like the definition by Cambridge Dictionary, describing risk as the possibility of something bad happening.

It perfectly encapsulates the two key aspects of risk (and thus, risk management): First, that risks are something bad, whether that is a simple inconvenience, risk of capital, or even risk of life. Second, that risks are a possibility of the occurrence of a negative event, meaning that there is some probability involved of that risk happening, not happening, or perhaps happening at different levels of intensity.

And while this definition of risk itself is (in my view) universally true, the perception of certain risks, as well as the resulting attempts at risk management, are extremely subjective.

Fundamentally, this is driven by the simple truth that nobody can fully predict the future. Even the smartest investors in the world can only build models that try to predict (risk) events. And even having a correct model does not mean that an investor might correctly predict how other (market) participants react to the occurrence of a correctly predicted event.

Beyond this simple truth, the subjectivity, in my view, arises from two key points:

First, by the probability that an investor assigns to the occurrence of a certain risk event. Outside of certain idiosyncratic risks, we are all subject to the same types of risks, whether those are risks that affect all of us equally (think a market drawdown or a change in interest rates) or risks that affect all of us independently (think illness or a car accident). Nevertheless, each of us might put different probabilities on the same event, and thus, might have varying views on whether to hedge certain risks - and if so, how.

This might be due to how our personal circumstances shape how certain risks affect us. If I don’t ride a car to work but just take the occasional cab, I would expect my probability of having a car accident to be lower than someone commuting to work by car each day. When I’m on the street, my risk of a car accident might be as big as anybody’s - but I might see the overall risk as less likely. Equally, an investor that doesn’t invest in certain emerging markets will likely not face the risk of regime change or other unfortunate events in said market.

But it also extends to certain events that, if they occur, would affect all of us equally. Take the very extreme example of the risk of nuclear war - how should you hedge yourself (and your portfolio) against such a catastrophic event? If you find it very improbable, despite its fatal consequences, you might choose to be unhedged against such a risk. Take Peter Berezin of BCN Research, who argues that there aren’t really any realistic ways to hedge yourself against such a risk from a financial perspective - but also, that it is not needed, given that your portfolio (and any other asset) would likely go to zero. Yet others might find it more likely and look for hedges to such an unhedgeable event - for example, by becoming a ‘prepper’ or even building a bunker.

Second, by the impact of the occurrence of a risk event in the investor. This is especially driven by an investor’s Investment Objectives. Take the risk of a market drawdown: One investor might be extremely long-term oriented and more focused on achieving their long-term return. Another investor might have short-term liabilities, making them unable to take significant hits. Both investors might have the same equity exposure in their portfolio, meaning that they would be equally impacted (within that equity allocation) by a drawdown - yet for the second investor, the occurrence of the event would have a much more severe impact, meaning they need to think differently about how to avoid or mitigate such a risk.

Categorizing Risk

Measurement of impact and estimation of probability of a risk event, taken together, allow us to get a good understanding of how an individual risk event would affect us. But having the tool alone doesn’t help us, of course: We need to think about what risk factors there are, to then use the tools at hand to quantify their impact on ourselves.

I could try to list some of the typical investing-related risk factors you read about, whether it is in the disclaimer section of a private equity fund or the quarterly report of a publicly listed company. That would likely take up a lot of time, and not be a lot of use to you. So instead, I’d like to suggest the following framework:

Let me explain my thinking to you.

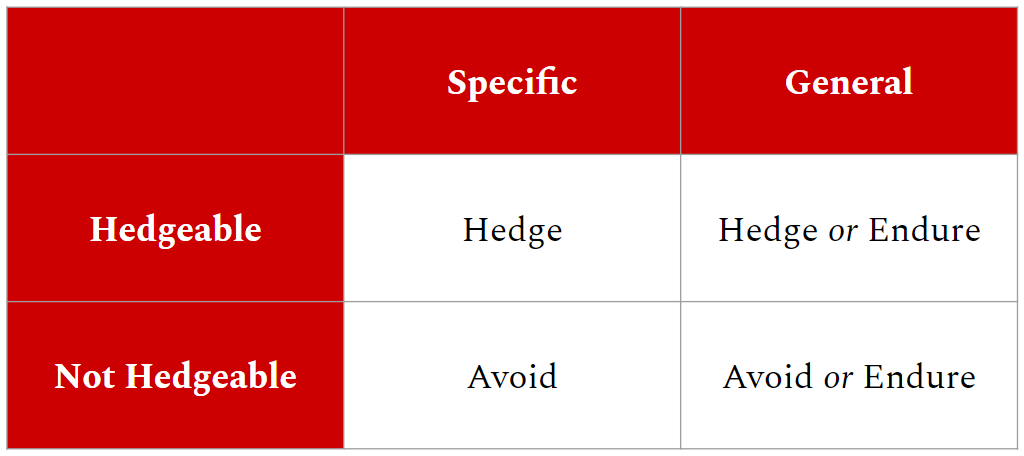

Specific Risks: Risks that affect you as an individual person, investor, or company, often independently from occurrence of the same (or a similar) risk event in another person, investor or company.

General Risks: Risk that affects all persons, investors, or companies, equally.

Hedgeable Risks: Risks against which an investor can make specific measures to either reduce the impact of the specific risk event, or which result in avoiding the risk entirely. (It’s important to note that a hedge impacts the effects of a risk event on the individual, but does not reduce the occurrence of the risk event.)

Non-Hedgeable Risks: Risks for which there are no specific measures or methods that reduce or avoid the impact of said risk.

Taking these two variables together, we get a neat little framework to think about various risks, and how we should think about dealing with them. Let’s consider an example for each category.

Specific, Hedgeable Risks: Those are risks that affect you as an investor specifically and independently, but to which there are ways and methods of hedging this risk. An example would be fire insurance for your house: It is very likely that a fire in your house would only affect you, but luckily, this specific risk can be hedged through (an often affordable) insurance policy.

The best approach to specific, hedgeable risks, in my view, is to actually hedge them: Given their independent nature (i.e. if the event happens, it just happens to one individual, and not all of the individuals theoretically affected by such risks), hedges are typically cheap and worth their money, as for example is the case with many (but not all) insurance policies.

Specific, Unhedgeable Risk: Specific, unhedgeable risks affect you individually and independently, but have no method on hand that would allow you to reduce the impact of said risk event. Unlike the prior category, such risks might have prohibitively expensive hedges, or might not have any available hedges at all. An example here would be flood insurance for a property in a flood-endangered zone: Insurance might not be available at all, or only at extremely high rates.

The best approach to such risks is to avoid them: Given that they often would have significant impact, but cannot be protected against, the best path is simply not to play - unless the ‘reward’ side of the equation is worth the often substantial risk.

General, Hedgeable Risks: Such risks affect all participants equally, but there are ways to mitigate against such risks. An easy example here is the risk of a market downturn, hedged through put options: Any market participant can go and buy short- or long-term protection in the option markets.

There are two approaches to such risks. One is to simply hedge them - as is the case with buying put options. However, hedges for such general, hedgeable risks might often come at a price: Given that occurrence of the risk event might affect many participants equally, the providers of risk protection (i.e. the put sellers) often let themselves be paid considerably - and as I mentioned before, investors cannot forecast when a market downturn will happen, so they might need to maintain the protection for a long time without guarantee of the protection actually paying off at some point (let alone recouping the cost of prior periods).

The alternative is to simply endure a risk. While extremely dependent on the actual risk (nuclear risk being a general, yet very negative event), many general risks, especially when it comes to market-related risk, tend to be temporary. They are not an existence-threatening, singular event like house fire or disease. Instead, they are - as I outlined in my introduction - the fundament of generating returns: It’s such general risks such as market and economic developments that, if taken, might allow investors to see positive performance.

General, Unhedgeable Risks: Such are risks that affect all participants equally, but against which an investor cannot (completely) protect themselves. Many risks in this category are the fundamental basics of investing - the most basic one being that no investor (outside the examples in my introduction) has the guarantee that they will generate returns on their investment.

Again, there are two approaches, both of course being specific to the individual risk factor. The easiest way to deal with general, yet unhedgeable risks, is to simply avoid them: If you cannot for example stomach more than a certain percentage loss on your invested capital, you should avoid investments (or entire asset classes) that might realistically see such a loss in a market downturn.

The other alternative, once again, is to endure such risks. Take the fundamental truth of risk-reward: No investor has a guarantee that they will make money, even though history has given us somewhat of an indicator that some of the basic truths (like a positive return on equity risk) might also hold true in the future. As we just stated, one way is simply not to play - but the equal option might be to simply endure those risks, and hope for the best, as long as the statistical odds are somewhat in your favor.

What Risks To Take?

Using both those variables, and the methods of impact and probability, we have a great set of tools to get to work on our individual risk identification and risk management frameworks.

As I mentioned, identifying and dealing with risk tends to be an extremely subjective matter. It is framed by your individual Investment Objectives, as well as your personal view of risks and their impact.

You might wonder: Jan, things are subjective, but in general, what risks do you think are worth taking - and which ones are not? It is something that I think about a lot, not only specific to topics of interest such as private equity, but also beyond the investment portfolio - the latter being something that many (affluent) individuals underestimate.

And I’d be happy to share my views with you - but that’s for next week’s newsletter.

Liked what you read? If you enjoyed this piece, make sure to subscribe by adding your email below. I write about topics covering the world of family offices, asset allocation, and alternative investments.